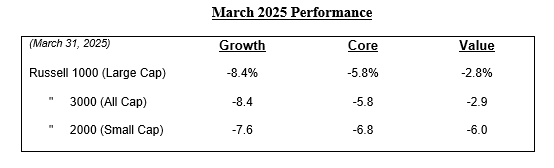

U.S. stocks dipped lower in March as the S&P 500 suffered its worst monthly decline since December 2022. Broader economic uncertainty and recession fears continued to pressure growth and tech stocks, with the market decline fueling a flight-to-safety.

The market continues to digest the policies and tariffs proposed by President Trump. Both companies and investors are debating whether these tariffs are merely a negotiating tactic or if broad-based tariffs will become a defining feature of his presidency. More recently, Trump announced additional 25% tariffs on all cars manufactured outside of the U.S. and hinted that the widely anticipated April 2nd reciprocal tariffs will be “very lenient”.

Adding to the uncertainty, declining small business sentiment, remarks from Trump’s antitrust officials, and recent bank updates on capital markets have all weakened the post-election bullish narrative centered on deregulation and animal spirits.

On March 19th, the Federal Reserve held interest rates steady but still projects two rate cuts later this year. In addition, the Fed lowered its collective outlook for economic growth and slightly increased its inflation projection. Fed Chairman Jerome Powell noted that consumer spending has moderated and expects tariffs to exert upward pressure on prices. The next FOMC meeting is set for May 6-7.

Small- and mid-sized companies continue to trade at historically wide valuation discounts relative to their large-cap counterparts. Structural factors such as increased M&A activity, reshoring, insulation from multinational dynamics, declining interest rates, shifts in corporate tax policy and deregulation create a compelling landscape for selective opportunities.

The valuation of the Russell 2000 Value remains compelling, currently trading at ~12x estimated earnings for the next twelve months versus ~21x for the S&P 500. This attractive valuation differential underscores the importance of valuations as a strong determinant of long-term performance.

As value-oriented stock pickers, we find the current market conditions exceptionally favorable for our methodology. Our focus remains steadfast on identifying exceptional businesses trading at a discount to Private Market Value, with catalysts to surface value. We will continue to use the volatility provided by Mr. Market to increase our stakes in great companies at attractive prices.