COMPANY OVERVIEW

Berkshire Hathaway Inc., based in Omaha, NE is a holding company for a diverse group of operating subsidiaries including insurance, freight rail transportation, utilities and energy, finance, services and retailing. The subsidiaries operate in an autonomous fashion, while investment and capital allocation decisions are managed by Warren Buffett (94) and Greg Abel (62) supported by investment managers Todd Combs (54) and Ted Weschler (62). Vice-Chairman, Ajit Jain (73) overseas risk capital for the insurance operations. As of December 31, 2024, since 1965, the firm had an annual compounded gain of 19.9%.

Berkshire Hathaway held its 60th annual meeting on May 3. Warren Buffett hosted with support on stage from Vice Chairmen, Greg Abel and Ajit Jain. Q&A alternated between Becky Quick from CNBC (emailed questions) and questions from the audience. We estimated that the CHI Health Center was completely full at its ~18,000 capacity and a total of 40,000+ in the city of Omaha.

Major Announcements – Buffett to Step Down as CEO

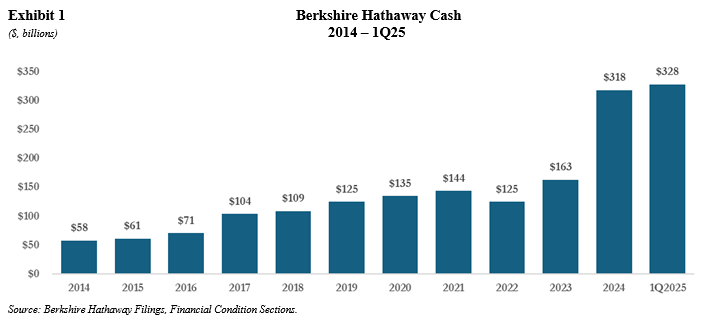

During the meeting, the company reported net earnings of $4.6 billion vs. $12.7 billion (YoY) with cash rising $10 billion in the quarter to $328 billion (Source: 1Q25 10-Q, Pg. 44). GAAP Book value increased $5.1 billion to $654.5 billion or ~$452,000 per “A” equivalent. At the very end of the meeting, Warren communicated that he would recommend to the Board that Greg Abel take over as CEO at the end of 2025. There was an immediate standing ovation by the audience with Warren stating, “the enthusiasm from that response can be interpreted two ways!” Subsequently, the Board approved Greg as CEO, with Warren retaining the role as Chairman. “I could be helpful, I believe, in certain respects if we ran into periods of great opportunity or anything. I think that Berkshire has a special reputation that when there are times of trouble for the government, we are an asset and not a liability, which is very hard to have because usually the public and government get very negative on business if there’s a time like that. But Greg would have the tickets. Whether it’s acquisitions – I think the board would be more welcome to giving him more authority on large acquisitions probably if they knew I was around. But Greg would be the chief executive, period.”

Of note, this was another brilliant example of handling a major situation for Berkshire. Ending the meeting with the announcement while retaining the secrecy meant he came public with this important news without any speculation or fanfare ahead of the meeting. This allowed him also to address questions and enjoy the engagement with shareholders without the succession overhang. He has always created great, positive Berkshire theatre and this deserved another Oscar as well as consideration for a lifetime award.

Shareholders should welcome this transparent transition, but also have confidence that Warren isn’t going anywhere. Retaining the position of Chairman means he can continue to mentor Greg and the Berkshire leaders, while also providing additional intellectual capacity when the inevitable time for more major capital allocation occurs.

There must have been a lot of pressure on Warren personally ahead of making the announcement. With this behind him and another meeting in the history books, Warren should benefit from the relief and more personal capacity to focus on what he loves – making Berkshire better and generating returns for shareholders.

Annual Meeting Highlights:

“Turn the Page.” I never dreamt of that when I picked up that handbook. It’s amazing what you can find when you just turn the page. We showed a movie last year about “turn every page,” and I would say that turning every page is one important ingredient to bring to the investment field. Very few people do turn every page, and the ones who turn every page aren’t going to tell you what they’re finding. So you’ve got to do a little of it yourself.”

- Cash levels. As of 1Q, cash and equivalents had increased to $328 billion. The sheer investment in short-dated Treasuries makes Berkshire approximately 5% of the total market. Ideally the managers would like to work down the capital to a lower balance but will be patient until the environment is most fruitful. “We are running a business that is very, very opportunistic.” Additionally, capital generation is about $40 billion per year and that will have be invested going forward. Based on the current large numbers, it is likely Greg Abel will preside over more capital allocation than during the previous history under Buffett. “The amount of cash we have – we would spend $100 billion if something is offered that makes sense to us, that we understand, offers good value, and where we don’t worry about losing money. The problem with the investment business is that things don’t come along in an orderly fashion, and they never will.”

- Tarriff/Trade Policies Trade policy should not be used as weapon. The United States should be looking to trade with the rest of the world. Warren believes in comparative advantage – there is a reason cocoa should be raised in Ghana and coffee come from Colombia. “The United States has become an incredibly important country starting from nothing 250 years ago – there’s never been anything like it. And it’s a big mistake when you have 7.5 billion people who don’t like you very well and you have 300 million people crowing about how well they’ve done. I don’t think it’s right and I don’t think it’s wise. The more prosperous the rest of the world becomes, it won’t be at our expense – the more prosperous we’ll become and the safer we’ll feel and your children will feel someday.”

- The concept of the American Tailwind remains intact despite recent volatility and political change in Washington. “If you don’t think the United States has changed since I was born in 1930, you’re not paying attention. We’ve gone through all kinds of things – great recessions, world wars, the development of the atomic bomb that we never dreamt of when I was born. So I would not get discouraged about the fact that we haven’t solved every problem that’s come along. If I were being born today, I would just keep negotiating in the womb until they said I could be in the United States. We’re all pretty lucky. We’ve got two non-United States guys (Greg Abel and Ajit Jain) here who now live in the US.”

- Japanese Investments. Berkshire has major holdings in five of the Japan “trading companies” including Itochu Corp, Marubeni, Mitsubishi Corp, Mitsui Co LTD, and Sumitomo Corp. The firm first started acquiring the positions (~10% each) about six years ago and in aggregate the total US notional is a little over $20 billion. They have been pleased with the performance and would like to own more of each and currently are working on relaxing the ownership caps (no more than 10%) with each. They really like the long-term opportunity and would be happy to own $100 billion in aggregate. As part of the investment, Berkshire issued Yen denominated debt (weighted average cost @ 1%) so a nice carry against current returns (dividend yields) that are higher than the 1%. This financing arbitrage was an added benefit to an already desirable risk/reward. Additionally, the allocations fit within the long-term mold, and they intend to hold for many decades, while also benefiting from other potential capital allocation opportunities through their friendly relationships with the Japanese companies.

- Over the last several years, Berkshire has bought in the remaining 9% of Berkshire Hathaway Energy that it did not own. The first major transaction was buying Greg Abel’s 1% stake for $870 million at a valuation of $87 billion (June 2022). More recently, the Nebraska company purchased the remaining 8% from the Scott Family for $3.9 billion which included shares of BRK’B (2.3m @ $456) at a valuation of $49 billion (September 2024). So why the major delta in valuation? First, utilities multiples have been impacted by trial award liabilities associated with West Coast wildfires. Second, BHE had a negative judgement settled for $250 million related to its real estate division, which came with the Mid-American transaction. Admittedly, Warren stated they erred in keeping the utilities together rather than parsing out state by state since there are different regulations and state attitudes that have developed around liabilities. On the positive side, energy demand will increase in the future and managing the grid will become a greater infrastructure importance. Warren believes that there should be a movement to a national authority to coordinate and manage the US grid, much akin to the effort to build the national highway system. Local regulations may make it too hard to be efficient with capital expenditure at a time when the US will need to address surging energy demand.

- AI and impact on insurance. Ajit Jain concluded that there is “no question that AI will be a game changer.” It will impact how the firm manages risks and paying out claims. Some of the industry is spending enormous amounts of money chasing the next “fashionable thing.”Berkshire will be cautious before committing to spending a lot. By not being a first mover, Berkshire will benefit from seeing how the landscape crystallizes and then will invest to stay competitive. Some insurance subsidiaries are using AI currently, but no big adoption yet. So the insurance segment is in a “state of readiness, and should that opportunity pop up, we’ll jump in promptly.”

- GEICO. Under the leadership of Todd Combs, the car insurance firm has made a strong turnaround including adapting telematics, adjusting rate policy to reflect risks and reducing headcount by 20,000 people for ~$2 billion of savings. For 1Q25, the GEICO unit generated a combined ratio of 79.8%, which is a large margin for insurance companies. Efficiency improvement remains a work in progress given the dynamics of the industry and the need for investment in technology. Despite a few historic instances of decreasing profitability, the business remains a gem for Berkshire. The first 50% was acquired in 1976 for $50 million. Last quarter, the fully owned unit generated $2 billion of EBT. Additionally, the insurance segment has $29 billion of investable float.

- Autonomy and impacts on insurance. “There is no question that insurance for automobiles is going to change dramatically once self-driving cars become a reality.” -Ajit Jain. Most of the insurance sold today is around operator error. Over time the industry share will change from operator liability insurance to more product liability driven coverage as passengers rely more on autonomy. In any case, GEICO will be well positioned to deliver insurance coverage and has enjoyed strong growth rates over time. In 1951, the average price of a policy was about $40. Today it is easy to get to $2,000 depending on location and requirements. During this time though, the number of people killed per 100 million miles driven has fallen from 6 to a little over 1 (WB). “So the car has become incredibly safer, and it costs 50 times as much to buy an insurance policy.”

- Despite the volatility in April and YTD, Warren does not believe it constitutes a real big move. There have been three times in Berkshire’s history when the shares declined 50% or more, and in a fairly short period of time. “Nothing was fundamentally wrong with the company any time.” In September 1929, the Dow Jones average declined to 42 from 381. By comparison the recent declines have not really been any kind of real bear market. Since Warren’s investing history there have been ~17,000 trading days and plenty of periods that were more dramatic than the last few months. There will be a “hair curler” event in the future because that is what markets do from unexpected events. But to be successful, you need the proper temperament for it – “I know people have emotions, but you’ve got to check them at the door when you invest.”

- In response to a question on good habits and succeeding in investments, Warren exclaimed with a familiar response. You must find what you are passionate about and then apply yourself, but you still need to be realistic about your core competencies. “I don’t believe in that book that talked about spending 10,000 hours at something. I could spend 10,000 hours at tap dancing and you’d throw up if you watched me. But if I spent 10 hours reading Ben Graham, I would be damn smart when I got through (it).”

Performance

Berkshire Hathaway continues to be among the largest public capitalizations in the United States. Since taking over Berkshire Hathaway in 1965, Mr. Buffett has generated an overall gain of 5,502,284% vs. the 39,054% change in the S&P 500 (including dividends). We would note that Berkshire’s performance is after-tax, while the S&P 500 return is pre-tax.

Cash Balances

Berkshire Hathaway has a long history of capital generation and productive capital allocation. At times the firm can act quickly and in a large fashion to invest in public equities, controlled businesses and or repurchase shares. During the financial crisis, Berkshire invested significant amounts in Bank of America (NYSE: BAC), Dow (NYSE: DOW), General Electric (NYSE: GE), Goldman Sachs (NYSE: GS), and Mars and which led to billions of future gains. At the end of 1Q25, cash had risen to $328 billion which if compared equal to capitalization would make it the 25th largest company in the S&P 500 Index.

Valuation

In the past, Mr. Buffett referred to Berkshire’s change in book value as one proxy for evaluating the progress against the S&P 500 Index. Since 2005, price-to-book (GAAP) value has fluctuated between 1.1x and 2.0x. At the end of March 2025, book value per Class A Share was $451,579 or about 1.8x the current price.

Repurchase Levels

For many years, Berkshire had a common share repurchase plan based on buying shares at prices no higher than a 20% premium to book value. On July 17, 2018, Berkshire’s Board of Directors changed the program. Now Warren Buffett (and previously with Charlie Munger) is authorized to repurchase shares when he believes shares are trading at a discount to intrinsic value, “conservatively determined.” Since the change, the company has repurchased 64,105 Class A Shares for $26.4 billion and 216 million Class B Shares for $51.3 billion. (Table 2) The average repurchase price per “A” and “B” was $411,111 and $237.11, respectively, compared to the current May 3 closes of $809,350 and $539.80. We estimate that since the beginning of the step-up in repurchases in 2018, the company has reduced outstanding shares “A” equivalent by ~200 million or 12%. We would note though that since 1H2024, the company has not repurchased any shares.

As part of the Inflation Reduction Act, corporations must now pay a 1% excise tax on all repurchases. In 2024, that was approximately $30 million for Berkshire. During the meeting, Warren highlighted that the cost of the tax would also be another element of consideration for repurchase levels and that current lobbies in DC are looking to raise that 1% further. Net/net, the normal discount to intrinsic value for buying back shares would have to include also the cost of any tax payments.

Macrae Sykes © Gabelli Funds 2025

msykes@gabelli.com