Reflections from Gabelli Funds’ 16th Annual

Media & Entertainment Symposium

Gabelli Funds hosted its 16th Annual Media & Entertainment Symposium at the Harvard Club in New York City on Thursday, June 6, 2024. The symposium featured discussions with leading companies and organizations across the media ecosystem, with an emphasis on industry dynamics, current trends, and business fundamentals, as well as a Sports Investing Panel. Attendees also had the opportunity to meet with management in a one-on-one setting.

Hanna Howard is a research analyst and covers both the packaging industry as well as the telecommunications sector with a focus on broadcasting and media companies. She joined the firm full-time in 2019 after completing an internship during the summer of 2018. Previously, she was an analyst at Steel Partners Holdings and an associate at Huron Consulting Group.

Hanna graduated cum laude from Vanderbilt University with a BS in human and organizational development. She also holds an MBA with a concentration in Finance from Northwestern University’s Kellogg School of Management.

Christopher Marangi serves as Co-CIO, Value and portfolio manager for several open/closed-end funds and separate accounts. He joined GAMCO in 2003 as a research analyst covering companies in the Cable, Satellite and Entertainment sectors. Chris began his career as an investment banking analyst with J. P. Morgan & Co and later joined private equity firm Wellspring Capital Management.

Chris has appeared on CNBC and Bloomberg television and radio and has been quoted extensively in publications including the Wall Street Journal, The New York Times, Barrons, Newsday, Bloomberg, Variety and Broadcasting & Cable.

Chris graduated magna cum laude and Phi Beta Kappa with a BA in Political Economy from Williams College and holds an MBA with honors from the Columbia Graduate School of Business.

Jenny Mu is a research analyst covering the global media sector with a focus on live entertainment, cable, and outdoor advertising. She joined the firm in 2023. Previously, she was a research analyst at Franklin Templeton Investments, and an institutional sales and trading analyst at BNP Paribas covering foreign exchange derivatives.

Jenny holds a BA in public policy from Princeton University and an MBA in finance from the Wharton School at the University of Pennsylvania. She is a CFA charterholder and a CAIA charterholder.

Justin McAuliffe joined the firm in 2021 as a research analyst covering the gaming and lodging sector as well as food retail. Previously, he served as Program-Related Investment Officer at the Conrad N. Hilton Foundation. Justin is a graduate of the Cornell School of Hotel Administration and has an MBA from the Marshall School of Business at USC.

Sergey Dluzhevskiy joined the firm in 2005 as a research analyst and is a co-portfolio manager of The Gabelli Global Content & Connectivity Fund, an open-ended mutual fund that invests in companies in the telecommunications, media and information technology industries. Prior to that, he was an equity research analyst at Loomis Sayles & Company. He began his career as a senior accountant at Deloitte & Touche.

Sergey graduated summa cum laude with a BS in accounting from Case Western Reserve University and holds an MBA with honors with concentrations in finance and accounting from Wharton School at the University of Pennsylvania. He is a CFA charter holder and a CPA.

Key Themes: Today’s Changing Media Landscape

Broadcasters’ revenue profiles are less dependent on advertising spending and less impacted by the rise of virtual MVPDs than cable networks. The landscape has evolved as scaled players have emerged from consolidation. Broadcasters have been aggressive at driving contractually-recurring retransmission fees, and political advertising dollars are again expected at record levels in the 2024 presidential election cycle. While core advertising is highly volatile during recessionary periods (during the 2008-2009 financial crisis, U.S. advertising saw steep declines of more than 15%), politicians and PACs are generally well-financed. Local TV should be the primary beneficiary of record 2024 presidential election cycle political ad spending, and given low variable costs, political ad dollars generally fall to a pure-play broadcaster’s bottom line. With contractually-guaranteed retransmission revenues and record political advertising spend expected in 2024 broadcasters are better-positioned to withstand a more challenged economic backdrop.

Cord Cutting & Shaving – Pressure Persists: From a peak of over 100 million in 2013, total pay-tv subscribers are now estimated to reach 73 million by year-end 2024, representing 60% household penetration (down from a peak of over 85%). In light of these shifts, the U.S. pay-tv landscape is changing. Virtual MVPDs are becoming increasingly prevalent as younger consumers continue to shave and cut the cord, and these services continue to take share from traditional pay-tv offerings. The growth in virtual MVPD subscribers has helped to offset some of the declines on the traditional MVPD side, although not fully. Retransmission revenues are backed by multi-year contracts, so unless there are a significant number of subscriber cancellations above prior expectations, which remains unlikely at this time, there should be little impact in a more challenged macro environment.

Core Advertising Trends: Broadcasting companies’ revenue will likely be negatively impacted, at least in the near-term, as a result of exposure to advertising. However, the impact is somewhat mitigated by broadcasters’ diversified sources of revenue today, as non-political (‘core’) advertising comprises less than 50% of a pure-play broadcaster’s revenues (as compared to about 90% during the last recessionary period). The economic outlook in the U.S. remains uncertain, and macro dynamics continue to have an impact on corporate advertising and marketing budgets, which are often viewed as discretionary.

2024 Political Advertising Outlook: In contrast to core advertising, U.S. political advertising is again anticipated at record levels during the 2024 presidential election cycle. Local broadcast stations remain uniquely positioned for political advertising given the regional nature of their signals. While digital continues to take share of the total U.S. advertising market, local TV still captures the lion’s share of total political ad spending. Competitive races typically generate the most political advertising revenue, and accordingly, stations reaching markets with those close races should outperform. Strong political this year should help mitigate lingering core advertising demand.

Broadcast Industry Regulations & M&A Activity: On April 20, 2017, the FCC reinstated the Ultra High Frequency (UHF) discount giving broadcasters with UHF stations the ability to add stations without running afoul of the National Ownership Cap. The current 39% ownership cap is unlikely to change in the near-term. Should the FCC substantially change the ownership cap, we would expect consolidation to accelerate. We would expect both cost reductions and revenue growth, primarily in the form of increased retransmission revenue, to benefit the broadcast stations and networks.

Streaming Wars & Content:

The streaming business is in transition. Companies across the industry are dialing back expectations for subscriber growth and the amount that they are willing to spend on content. So far, Netflix is the only streamer that has been consistently profitable at scale. The legacy media companies need to determine an economic model that will lead to profit sooner and offset the declines in their legacy broadcast and cable businesses. Advertising will play a bigger role in the future of streaming, whether that is in Free Ad-Supported TV (FAST) or Advertising-based Video on Demand (AVOD). Netflix, Disney+, Amazon Prime, and AMC Networks, among others have all launched AVOD tiers.

Outdoor Advertising:

The out-of-home (OOH) advertising industry is rapidly evolving, fueled by technological advancements and shifting consumer behaviors. Digital out-of-home (DOOH) advertising is projected to grow 12% in 2025, driving an overall OOH industry growth of 7%. Advanced measurement and attribution tools enabled by new technology attract new advertisers into the OOH space. Transit advertising, especially in airports, continues to be a growth area for OOH, supported by increasing air travel trends. As traditional advertising mediums like linear TV, radio, and print lose market share to digital platforms, OOH is poised to maintain or even grow its share due to its complementary role in digital campaigns.

COMPANY OVERVIEW

Beasley Broadcast Group, a multi-platform media company, owns and operates 57 AM and FM radio stations in 13 large- and mid-size markets across the United States. The company offers local and national advertisers integrated marketing solutions across audio, digital, and event platforms. It also operates Houston Outlaws, an esports team that competes in the Overwatch League, and an esports team that competes in the Rocket League. The company was founded in 1961 and is headquartered in Naples, Florida.

Reason for Comment

On June 6, 2024, Beasley’s CEO: Caroline Beasley, CFO: Marie Tedesco, and Chief Revenue Officer: Tina Murley presented at our 16th Annual Media & Entertainment Symposium. Highlights from the session are included below:

- Beasley stations reach more than 28 million consumers on a weekly basis. Roughly 40% of Beasley’s radio properties are located in the U.S. top 50 markets, with the remaining stations primarily in vibrant regional centers.

- Revenue from company’s foundational business, Audio continues to increase as a result of Beasley’s unique talent offering community-engaging content. BBGI’s stations are home to a diverse range of formats, featuring top on-air personalities and programming that appeal to a wide range of audiences/demographic groups. In terms of advertising exposure, ~70% of total revenue is local (including digital sold locally) and ~12% is national.

- Beasley’s Digital division combines the power of local with BMG’s industry-leading digital offerings to deliver results-driven integrated marketing programs for clients. BBGI expects digital to account for 20-25% of total revenue in 2024, driven by the ongoing growth and success of their premium content creation & digital services. On the new business front, the company’s dedicated sales teams (of over 200 people) are leveraging the tremendous audience reach and engagement of Beasley’s platform to attract new advertisers.

Summary

Beasley has positioned itself as the one-stop shop for all local business advertisements. The company’s radio clusters are some of the largest station groups in their respective markets (when ranked by revenue), which helps to enhance each station’s group appeal to the widest range of advertisers and generate operating efficiencies. The digital side of the business continues to see strong growth, and accounts for 20% of total company revenue today. Growth in 2024 and beyond will be driven by strategic investment into the expansion and enhancement of digital capabilities.

COMPANY OVERVIEW

Headquartered in Reston, Virginia, ComScore operates as an information and analytics company that measures audiences, consumer behavior, and advertising across media platforms in the U.S., Europe, Latin America, Canada, and internationally. The company offers a wide range of ratings and planning products and services; custom solutions for planning, optimization, and evaluation of advertising campaigns and brand protection; and provides products that measure movie viewership and box office results. It serves digital publishers, television networks, movie studios, content owners, brand advertisers, agencies, and technology providers.

Reason for Comment

On June 6, 2024, ComScore’s Chief Executive Officer, Jon Carpenter participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Highlights from the session are included below:

- Media disruption has upended the way marketers and media companies connect with audiences to drive growth, and a primary challenge today is accurately measuring audiences in an increasingly cross-platform world. Leading global businesses need an independent partner for understanding consumer behavior across platforms.

- SCOR believes it is uniquely positioned to deliver on the opportunity today because of its broader audience view and its experience analyzing that data. ComScore has the ability to measure audiences more granularly at the household level due to its focus on data (vs. panels), and is the only firm with a MRC accreditation. SCOR has ~25% market share of being used as a currency, mostly in local, or cross measurement, which shows that it is effective at competing against Nielsen.

- The company has made significant progress toward reducing the latency of its measurement results, with its traditional TV data now available within 48 hours, and digital data within one day, at a 95% accuracy level.

- SCOR completed a 1:20 reverse stock split on December 20, 2023. Further improving the capital structure and simplifying the balance sheet remains a high priority for the company moving forward.

Summary

ComScore plays an integral role in the media ecosystem today; with transformative data and vast audience insights across digital, linear TV, over-the-top (OTT), and theatrical, the company is a powerful third-party source for reliable measurement of cross-platform audiences.

COMPANY OVERVIEW

Clear Channel Outdoor Holdings, Inc. (NYSE: CCO) is at the forefront of driving innovation in the out-of-home advertising industry. The company’s dynamic advertising platform is broadening the pool of advertisers using the medium through the expansion of digital billboards and displays, the integration of data analytics, and programmatic capabilities that deliver measurable campaigns that are simpler to buy. By leveraging the scale, reach and flexibility of their diverse portfolio of assets, the company connects advertisers with millions of consumers every month.

Reason for Comment

On June 6, 2024, Clear Channel Outdoor’s Chief Financial Officer, David Sailer, and Chief Revenue Officer, Bob McCuin, participated in a fireside chat at our 16thAnnual Media & Entertainment Symposium. Highlights from the session are included below:

- Digitization of CCO’s inventory continues to be a driver of organic growth. Programmatic OOH is a small but growing part of the business. The programmatic opportunity for CCO currently is in filling out digital inventory outside of direct buys.

- Strength in out-of-home has been predominantly local, while national still lags. Weaker verticals like Media & Entertainment are rebounding, while Business Services remains strong on the local side.

- CCO’s RADAR platform allows advanced data analytics like measurement and attribution based on location-services data to measure consumer exposure to displays, footfalls, app downloads, and store visits. The data insights allow CCO to go after new verticals like Pharma, CPG, and Beverage.

- CCO is currently in the process of selling its Europe North and LatAm assets. The proceeds will be used to pay down its outstanding $365 million CCI B.V. notes and will allow CCO to focus on their higher-margin America business and grow EBITDA organically.

Summary

As one of the largest OOH companies in the US, CCO should benefit from overall growth in the OOH industry driven by technological innovations in digital OOH and programmatic channels. Leverage remains an overhang on the stock, but CCO should be able to organically delever from digital OOH growth, improved data analytics capabilities, and divestment from international assets to focus on the higher-margin U.S.

COMPANY OVERVIEW

Entravision operates a global digital marketing business and owns/operates 47 TV and 43 audio stations primarily targeting Hispanic consumers in the U.S. The company has three main businesses today: U.S. Media, including TV, radio, and digital (primarily Spanish language); Smadex, a demand side programmatic ad platform that specializes in mobile app user acquisition using AI); and Adwake, a programmatic ad services business, similar to Smadex, but with third-party technology. Entravision was founded in 1996 and is headquartered in Santa Monica, California.

Reason for Comment

On June 6, 2024, Entravision’s CEO, Michael Christenson presented at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- Entravision was founded as a Spanish language broadcaster 30+ years ago. Roughly 8 years ago, the company made a major pivot into digital marketing through a series of acquisitions, and EVC’s new management team is in the process of cleaning up the aftermath of this transition.

- In April, shares declined significantly following an announcement that Meta plans to take its ad sales in-house, ending its relationship with EVC and all its sales partners by July 1 materially reducing both the company’s revenue and EBITDA. EVC subsequently initiated a review of its operating strategy & cost structure.

- Linear TV is EVC’s largest focus, despite market pressures. The company’s Univision affiliate agreement ends in late 2026, and it is considering alternatives. EVC’s station portfolio is well-positioned to benefit from record political spending anticipated in 2024. Roughly 34% of Latinos are in six western states highly influential during elections, and 28% of voters are Latino, making them politically crucial. To help capture these dollars, EVC has recently doubled news time on stations. Radio faces similar challenges to linear TV, but performs well locally.

- Digital marketing runs through The Trade Desk, with potential to leverage Smadex. With over 2,000 funded Ad Tech companies in the space today, EVC anticipates further industry consolidation, from which it could benefit.

Summary

Entravision is undergoing a significant transitional period following the loss of a major digital marketing customer earlier this year. However, the loss of revenue associated with this relationship is expected to be partially offset by increased sales from higher political ads this election year, and EVC’s strong balance sheet should allow it to withstand near-term earnings pressure. EVC is also likely to be a beneficiary of further consolidation in Ad Tech.

COMPANY OVERVIEW

The E.W. Scripps Company is a diversified media enterprise and one of the largest independent owners of local television stations in the U.S. Scripps has nearly doubled its local TV station portfolio in the last several years, and the company’s Local Media segment operates more than 60 stations in 40+ markets across the country today, reaching ~25% of U.S. TV households. The Scripps Networks division is comprised of 8 national news & entertainment networks that reach nearly every U.S. household over the air, but they’re also widely distributed on pay-tv and connected TV. Scripps is the nation’s largest holder of broadcast spectrum. The company is also the longtime steward of the Scripps National Spelling Bee. The company was founded in 1878, and is headquartered in Cincinnati, Ohio.

Reason for Comment

On June 6, 2024, Scripps’ CFO, Jason Combs and Chief Communications & IR Officer, Carolyn Micheli participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- Scripps’ top priority this year is reducing debt and optimizing the company’s capital structure to move it further down to a level of leverage it is more accustomed to.

- SSP has publicly announced that a process was underway to explore the sale of the Bounce TV network prompted by increasingly strong inbound interest from qualified potential buyers. This is entirely consistent with Scripps’ long history of buying/creating businesses, growing the assets’ value, and then divesting at the right time for a strong ROI. Scripps is also exploring the sale of some smaller, non-strategic real estate assets.

- The DR marketplace continues to make a comeback in terms of both inventory demand and advertising rates. It was up for the quarter for the first time in two years, and it accounted for more than 40% of SSP Networks’ ad revenue. Scatter pricing was a good story in the Q1 as well, up nearly 40% vs. pricing in last season’s upfront.

- Political advertising is expected to be robust again industry-wide in 2024. SSP anticipates local political ads revenue of $240-270 million for the full-year (the high end of range is above 2020 political of $265 million).

Summary

While the recent softness in advertising spend, especially on the national side, has created challenges for the business, Scripps is better-positioned to weather an advertising recession today than in prior periods. The company has solid visibility into its contractually-backed retransmission revenues for the next several years, and the industry continues to expect record political spending during the 2024 presidential election cycle.

COMPANY OVERVIEW

Gray Television, headquartered in Atlanta, GA, is one of the nation’s largest local TV broadcasters, with high-quality stations serving 114 markets that reach ~36% of all U.S. TV households. In 2019, the company nearly doubled its size through the acquisition of Raycom and, in 2021, expanded further with the acquisitions of both Quincy Media and Meredith’s local TV station portfolio. Gray also owns video program companies Raycom Sports, Tupelo Media Group, PowerNation Studios, as well as the studio production facilities Assembly Atlanta and Third Rail Studios.

Reason for Comment

On June 6, 2024, Gray’s Chief Financial Officer, Jim Ryan and EVP Finance, Jeff Gignac participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- As of March 1, 2024, Gray completed retransmission renewals representing more than 70% of its traditional MVPD subscriber footprint in its current three-year retransmission renewal cycle. Retrans renewals have met Gray’s financial expectations, and all negotiations were completed without blackouts.

- The highly polarized political landscape and number of competitive races is anticipated to drive high-margin political ad spending industry-wide, and Gray has a strong footprint for the 2024 cycle. While GTN is not providing political guidance yet, we expect it to be close to the $600 million in 2020 (excluding the GA runoff).

- Gray has substantially completed construction of its Assembly Studios real estate complex located in the Atlanta metro area. NBCU has commenced a long-term lease for roughly two-thirds of this 43-acre facility, with the remainder now offered to third-party content producers on the spot market. Infrastructure has also been largely completed on an additional 80 acres across the remaining portions of the project, which is expected to be further developed into a mixed-use complex over the next several years. The project is now contributing to cash flow.

- Gray recently closed a refinancing of its $1.15 billion term loan due in 2026 and upsizing of its revolving credit facility, completing its refinancing process. With no maturities now until May of 2027, the focus will hopefully shift towards industry trends and deleveraging efforts. Gray is focused on deleveraging into the low-4x range.

Summary

Gray’s stations are typically the #1 or #2 in the markets where it operates, and the company’s strong rankings position it favorably both with advertisers as well as distributors and networks. The next big focus is near-term free cash flow and deleveraging from the 2024 political cycle.

COMPANY OVERVIEW

Lionsgate (LGF’A/’B) encompasses world-class motion picture and television studio operations as well as the STARZ premium global subscription platform. Lionsgate Studios (LION), which is comprised of Lionsgate’s Motion Picture Group and Television Studio segments along with a 20,000+ title film and television library, recently launched as a separate publicly-traded company on May 14, 2024, with parent Lionsgate continuing to hold an approximately 87% stake. Lionsgate’s corporate headquarters are located in Santa Monica, California, and it is domiciled in Canada.

Reason for Comment

On June 6, 2024, Lionsgate’s President of Worldwide Television Distribution, Jim Packer and VP Investor Relations, Nilay Shah participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Key highlights from the discussion are included below:

- Lionsgate’s TV and film businesses were recently combined with Screaming Eagle Acquisition Corp., resulting in the launch of a standalone public studio company through a SPAC IPO, of which LGF parent continues to own ~87%. This transaction valued the Studio business at 10.7x pro forma 2025P EV/EBTIDA.

- Lionsgate remains committed to the planned full tax-free separation of its Starz and Studio assets by the end of this calendar year. When Lionsgate was previously a pure-play, it traded in the low- to mid-teens multiple range, so management anticipates the standalone studio business will trade better than it does coupled with Starz today.

- In December, Lionsgate closed the acquisition of eOne, and it is already deepening the company’s library, strengthening the company’s Canadian production initiatives, diversifying the television group, and allowing it to efficiently scale Lionsgate alternative television into an unscripted powerhouse.

- Lionsgate’s capabilities in producing distinctive series and movies have produced a robust library of content. Library revenues totaled $886 million in the trailing 12 months, up slightly vs. year-end fiscal 2023 levels.

Summary

Lionsgate’s recent Studios transaction increases transparency for that business and helps lower net leverage following the recent eOne and 3Arts purchases. The company also closed the bond exchange, which provides greater flexibility in managing corporate debt. These two transactions will help propel Lionsgate towards a full separation of the Studio and Starz businesses, still anticipated to occur before calendar year-end. We anticipate there will be M&A interest, especially in Studios, following the separation. Similar assets have historically transacted at ~12-13x EV/EBITDA.

COMPANY OVERVIEW

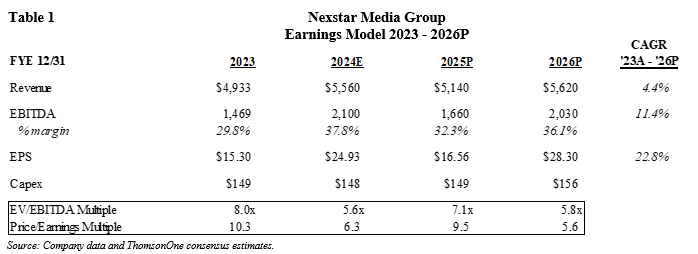

Nexstar Media Group, headquartered in Irving, Texas, is the largest local broadcast television group in the United States. The company owns or operates 200 TV stations in 116 markets, reaching 39% of U.S. TV households (after applying the FCC’s UHF discount). Nexstar also owns NewsNation, a recently-acquired 75% ownership interest in The CW (the fifth major broadcast network in the U.S.), two digital multicast networks, and a ~31% ownership stake in TV Food Network, The company’s digital assets include 120 local websites and 239 mobile applications, national digital properties including NewsNationNow, The Hill, BestReviews, and a suite of advertiser solutions.

Reason for Comment

On June 6, 2024, Nexstar’s President & Chief Operating Officer, Michael Biard and Chief Financial Officer, Lee Ann Gliha participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- Local core advertising has remained relatively resilient, and Nexstar is seeing increasing spending across most categories. NXST is also starting to see a recovery in both the general national network and DR marketplaces.

- Nexstar expects full-year 2024 political revenues will exceed both 2020 and 2022 levels. Given Nexstar’s extensive footprint covering almost 90% of contested elections, the company is extraordinarily well-positioned to take share and dollars, both locally and nationally.

- On a full-year basis, management has guided gross retransmission revenues growth in the high-single digits %’s, with net retransmission up in the low-teens range. Looking ahead, as networks continue to deemphasize linear, reverse compensation payments will continue to come down.

- NewsNation officially transitioned to a 24/7 news network on June 1st, and the CW is better-positioned than ever to capture advertising dollars moving forward by leading with sports and unscripted programming.

Summary

Nexstar benefits from industry-leading scale in linear television and an attractive station portfolio. The company has aggressively driven contractually-recurring distribution fee revenues, reducing its reliance on core advertising, which tends to be more volatile. In terms of 2024 political, Nexstar has one of the strongest footprints relative to contested races and ballot initiatives. A strong political cycle result will allow NXST to not only remain aggressive in terms of repurchases, but also continue debt pay-down on an industry leading balance sheet to help manage free cash flow.

COMPANY OVERVIEW

Rogers Communications, headquartered in Toronto, ON, is a diversified communications and media company that owns the largest national wireless service provider (11.5 million customers) and the largest cable MSO (4.2 million broadband connections) in Canada, as well as a media business with a focus on sports and regional TV and radio (including ownership of Toronto Blue Jays and a 37.5% stake in Maple Leaf Sports & Entertainment (owner of the Toronto Maple Leafs, Toronto Raptors, Toronto FC, etc.)).

Reason for Comment

On June 6, 2024, Rogers Communications’ President and CEO Tony Staffieri participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- Management has been pleased with acquisition of Shaw Communications (April 2023). The company was able to achieve C$1 billion synergy target one year ahead of schedule. The deal expanded Rogers’ bundling footprint, and now Alberta and British Columbia are its fastest growing markets.

- In wireless, RCI remains focused on network leadership and capturing market share with its flagship Rogers brand. While the firm puts less emphasis on flanker brands, it continues to do well in “New to Canada” segment (capturing ~2/3 market share within this customer category).

- Rogers expects exiting 2024 with a return to cable revenue growth. Principal drivers for top line improvement include growing broadband share within its cable footprint, increasing penetration with small- and medium-sized businesses (as combination with Shaw improved competitiveness in enterprise solutions), as well as addressing one-third of Canada (outside of its incumbent cable footprint) with fixed wireless access and broadband resale (bundling those services with wireless).

Summary

Recently completed acquisition of Shaw Communications (a) significantly enhanced the company’s scale, (b) provided access to deep fiber plant across Western Canada (which should help with network densification and improve competitiveness in enterprise solutions), (c) expanded the footprint where RCI could bundle wireless and wireline services (which drives churn reduction), and (d) put the firm in a position to generate meaningful synergies. The firm’s ownership of premier sports assets in Canada (Toronto Blue Jays and 37.5% stake in MLSE) could present opportunities to surface value over medium-term.

COMPANY OVERVIEW

Ryman Hospitality Properties, headquartered in Nashville, TN, is a lodging REIT focused on large group-oriented destination hotel assets. About three-quarters of Ryman’s room nights are filled by groups, with the remaining being leisure transient. Their core lodging portfolio consists of six upscale, meetings-focused resorts totaling 10,919 rooms, managed by Marriott under the Gaylord Hotels and JW Marriott brands. Five of their resorts feature in the top 10 largest in the US by square feet of self-contained meeting and exhibit space, with 2.8 million square feet of meeting and convention space in total across their portfolio. The Company also owns 70% of the Opry Entertainment Group (OEG), a taxable REIT subsidiary focused on the country music consumer. OEG owns two iconic live entertainment venues in Nashville, the Grand Ole Opry and Ryman Auditorium, as well as Block 21 in Austin, home of Austin City Limits at the Moody Theatre. OEG also owns seven live entertainment restaurant concepts in partnership with country music stars Blake Shelton and Luke Combs.

Reason for Comment

On June 6, 2024, Ryman’s Executive Chairman, Colin Reed, and Chief Executive Officer of the Opry Entertainment Group, Patrick Moore, participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- OEG is taking share in the fast-growing country music segment, estimated to have more than 150 million fans. Some of the short-term growth areas within the OEG portfolio include the renovation and rebranding of the Wildhorse Saloon into Category 10 in partnership with Luke Combs. The initial project will be a $40 million investment and feature a 1,500 seat ticketed venue and generate incremental revenues from a new seven thousand square foot roof deck. OEG is also renovating the W Hotel at Block 21 in Austin and recently opened a new Ole Red location on the Las Vegas Strip.

- Management also provided an update on the partnership with minority investor Atairos/NBCU. Last year, OEG launched the People’s Choice of Country Awards and Christmas at the Opry, which were distributed on NBCU platforms and won #1 or #2 ratings for national broadcast. NBCU has also started to distribute Opry Live content on their network and there is further potential to distribute content internationally through Sky Arts. NBCU is a preferred but not exclusive distribution partner, and Opry Live continues to be viewed by approximately 50 million households every week through syndication partner Gray Television.

- Ryman’s lodging segment continues to benefit from strong demand and limited supply supporting pricing power. Over the next four years, Ryman is targeting EBITDA growth at an 8.3% CAGR, supported by mid-single digit increases to average daily rates.

Summary

Ryman is the only REIT which focuses on the attractive niche of large group travel, which provides more visibility into future business, recurring revenue characteristics, and low volatility of earnings. Ryman’s “all-under-roof” model allows them to capture the majority of out of the room spend for group travelers, generating $1.50 of non-room revenues for every $1 of room revenues. As the only REIT focused on this segment, Ryman has purpose-built assets to cater to large groups which peers cannot easily replicate given the structural limit to new supply.

COMPANY OVERVIEW

Sinclair, Inc. is a diversified media company and a leading provider of local news and sports in the U.S. The company owns, operates and/or provides services to 185 television stations in 86 markets affiliated with all the major broadcast networks, and owns Tennis Channel and various multicast networks. Sinclair’s content is delivered via multiple platforms, including over-the-air, multi-channel video program distributors, and the nation’s largest streaming aggregator of local news content, NewsON. Sinclair was founded in 1971 and is headquartered in Hunt Valley, MD.

Reason for Comment

On June 6, 2024, Sinclair’s Chief Financial Officer, Lucy Rutishauser participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- Following Sinclair’s corporate restructuring in 2023, the company operates in two primary lines of business – Local Media, the broadcast business, and Sinclair Ventures, a portfolio of assets that includes Tennis Channel, Compulse (a digital marketing platform), and Sinclair’s investment portfolio. Sinclair continues to invest in news and content and make other investments around its core business and adjacencies including gamification, e-commerce, and the ground-breaking NextGen Broadcasting, expected to grow exponentially over the next decade.

- Sinclair has settled all Diamond Sports-related outstanding litigation claims. Now that this settlement has been paid, there should be no impact to Sinclair with whatever happens to Diamond in the future.

- In terms of the current ad environment, Sinclair is seeing strength across retail, services, entertainment, and sports betting categories, while medical and pharma pacings have softened a bit. Auto is trending slightly negative. Sinclair continues to anticipate >$350 million in political in 2024, a record excluding the 2020 Georgia run-off.

- Through early-May Sinclair has renewed retrans agreements covering 42% of Big-4 subscribers. Subscription revenue growth is expected to accelerate in the back half of the year given the timing of recent renewals, and management reiterated expectations for net retrans revenues to be up a mid-single digit CAGR from 2023-2025.

Summary

Sinclair anticipates 2024 will be a strong year driven by stable core advertising, robust political ads, and distributor renewals. Management continues to believe that today’s current valuations do not reflect the full intrinsic value of Sinclair’s robust set of assets, and are confident that over time, the company will be able to unlock unrecognized value as well as enhance the efficiency and effectiveness of Sinclair’s different strategic plans and operations.

Sports Investing Panel: A Golden Moment for Teams? Symposium Highlights

We hosted Michael Ozanian, Assistant Managing Editor of Forbes Media, and Michael Levine, Co-Head of CAA Sports for an engaging discussion on current trends in the sports business landscape.

Key Takeaways

- The pipeline of team transactions remains robust and franchise values continue to rise due to a scarcity of supply and a growing universe of buyers. Interest by private equity and sovereigns remains high. Leagues are likely to accommodate an increasing institutional presence with the NFL (the last of the Big 4 to prohibit private equity ownership) possibly loosening restrictions in the near term.

- The ratings dominance of live sports is driving ever-higher national media rights deals including for the NBA. Local sports rights remain valuable but regional sports networks (RSNs) are a work in process due largely to misaligned capital structures (e.g. Diamond Sports). Rights will migrate to some combination of healthy RSNs, local broadcasters, Big Tech and the leagues themselves. Leagues continue to balance maximizing audience reach and near-term revenue. Expect Big Tech – Netflix, Amazon, Google, Apple – to continue their foray into sports.

- Hospitality and real estate development will become higher proportions of revenue and value for US sports teams. F1 is a good example of what can be done with high-end hospitality while The Battery (the multi-use development surrounding the Atlanta Braves’ Truist Park) serves as a blueprint for other potential developments. Franchise buyers are increasingly considering real estate development potential as an element of price paid.

- Sports betting is a double-edged sword. It drives engagement, and helps draw younger viewers with shorter attention spans. However, betting by players could threaten the credibility of the game while an over reliance on sports betting advertising (particularly to the extent it targets minors) could endanger league/team brand equity.

- The NFL remains the most valuable league given its underpinning by national television contracts with games that account for over 50% of the top 100 broadcasts last year. Soccer valuations are trickier since teams are subject to relegation.

- Outside of the Big 4, Formula 1 and combat sports (e.g. UFC) have gained traction in the US. WNBA continues to build momentum which is spilling over into women’s soccer and women’s ice hockey. There’s value opportunity in women’s sports as they become an area of real growth. Upside in cricket, the third most popular sport in the world. Padel and pickleball have more commercial (e.g. court development) than professional potential.

Summary

We continue to view sports-related assets as excellent compounders of value. While local media rights disputes may have added noise to the value of baseball, hockey and basketball teams, consumer demand for this must-see live content remains strong. Newer revenue streams from sponsorship, hospitality, real estate and betting should support continued revenue growth while greater institutional interest in the sector is helping to surface franchise values. At the moment, public market opportunities to invest directly in US sports (Manchester United (MANU) trades in the US while a number of soccer franchises trade on exchanges throughout Europe) are limited to Atlanta Braves Holdings (BATRA/K), Madison Square Garden Sports (MSGS), Formula One (FWONA/K) and TKO Group (TKO).

COMPANY OVERVIEW

TEGNA Inc., headquartered in Tysons, Virginia, owns and operates 64 television stations and two radio stations in 51 U.S. markets. The company is the largest owner of Big Four network affiliates in the top 25 markets, reaching ~39% of all television households nationwide. TEGNA also owns leading multicast networks True Crime Network, Twist, and Quest. TEGNA offers innovative solutions to help businesses reach consumers across television, digital, and over-the-top (OTT) platforms, including Premion, the company’s OTT advertising service.

Reason for Comment

On June 6, 2024, TEGNA’s President & CEO, Dave Lougee and CFO, Julie Heskett participated in a fireside chat at our 16th Annual Media & Entertainment Symposium. Discussion highlights are included below:

- TEGNA has solid visibility into the company’s contractually-backed retransmission revenues through 2025. On the network affiliate side, the company renewed ~60% of its subscriber base at the end of the last year. Management reiterated that reverse comp growth should be ‘negligible at best’ from here.

- The industry is anticipating another record political cycle in 2024, and TGNA has a solid footprint. Additionally, the Super Bowl will return to CBS this year, and the Olympics will air on TEGNA-operated channels.

- TEGNA is the largest NBC affiliate owner, and when asked about the NBA possibly shifting to NBC, the company sounded positive about the possibility of NBC gaining a package of games, noting the uplift to ads of carrying the Olympics. While some issues would need to be worked out around scheduling, management was clear this would be a strong net benefit.

- TEGNA recently announced a cost savings plan that will amount to a $90-100 million run-rate by year-end ‘25. In the most recent quarter, Premion returned to positive growth despite the national challenges, and management expects this to accelerate through the remainder of 2024 and into 2025, especially when layering in Octillion.

Summary

TEGNA has solid visibility into the company’s contractually-backed retransmission revenues through 2025, and the industry continues to expect record political advertising for the 2024 election cycle. TEGNA has an industry-leading balance sheet, and expects to remain comfortably within the 2-3x’s leverage range, even after returning significant capital to shareholders following the termination of the Standard General merger process last year.

TV Bureau of Advertising (TVB) Panel Symposium Highlights

TVB OVERVIEW

TVB is the not-for-profit trade association representing America’s local broadcast television industry. Its members include the U.S. television stations, television broadcast groups, advertising sales reps, syndicators, international broadcasters, and associate members. TVB actively promotes local media marketing solutions to the advertising community and works to develop advertising dollars for the medium’s multiple platforms, including on-air, online, and mobile. TVB provides a diverse variety of tools and resources, including its website, to support its members and to help advertisers make the best use of local ad dollars

Reason for Comment

On June 6, 2024, TVB’s President & CEO, Steve Lanzano participated in a fireside chat at our 16th Annual Media & Entertainment Symposium to discuss trends, opportunities, & challenges in local broadcast television. Discussion highlights are included below:

- The advertising backdrop has been relatively stable overall. In terms of categories, auto is still between 17-19% a typical broadcasters’ business vs. >25% historically. Auto market supply is currently incredibly high, leading to increased incentives and lowered prices. Both dealers and manufacturers are focused on creating more demand, which should be a positive moving forward. Attorneys, which generally account for ~8-9% of the mix) are still spending, and the pharmaceutical category is benefiting more recently from advertising around weight loss drugs. Home improvement is also picking up, and the travel category has remained robust post the COVID slowdown.

- In terms of the sports betting category, which appeared as a bright spot a few years ago, 38 states have legalized it, but a few of the largest, including CA and TX, still have not. Typically, the category sees an influx of ad dollars when a new state opens up, so if any of the remaining large markets legalize, broadcasters should benefit.

- The intensely polarized political landscape and number of competitive races continues to drive high-margin political advertising spend industry-wide, and TVB is optimistic that 2024 political could approach or even surpass record 2020 levels. Forecasts have recently come up, and most are now anticipating roughly $11 billion in total political spending this year.

- Local TV is primarily a sports and news game today. Sports are likely the largest entertainment battleground as media, internet, and tech players vie for content. Local sports have been moving to local as DSG faces challenges, and leagues/teams balance revenue maximization with reach concerns as eyeballs move from linear to streaming.

- With respect to potential regulatory changes, TVB agrees with the consensus view that there are not likely to be any changes to existing rules near-term. Accordingly, large-scale broadcast M&A or regulatory changes are unlikely in the current environment. While the industry continues to believe that broadcast industry de-regulation is warranted, most do not anticipate any meaningful changes until there is a new administration.

- Another topic that continues to get attention is NextGen TV or ATSC 3.0, which is seeing continued momentum. Several use cases using the new transmission standard were discussed, including broadband data off-loading, and automotive applications related to over the air software updates and navigation. However, it will likely be at least several more years before the industry can begin to show material non-broadcast–correlated revenue and several years beyond that until it could potentially be a meaningful contributor. Barriers to more rapid scaling include chip set adoption, both in television sets (already slowly underway) and other end markets (automotive), as well as the related sun-setting of ATSC 1.0, which would free up more additional spectrum.

Summary

Local broadcasters are better-positioned to weather an advertising recession today than in prior periods, and TVB is seeing some positive momentum in terms of core advertising more recently. In addition, the industry continues to expect record political spending during the 2024 presidential election cycle. While larger-scale broadcast M&A and regulatory changes are unlikely in the current environment, this could change under the next administration. In addition, TVB continues to see a number of other opportunities for the local broadcast sector ahead, including NextGen TV or ATSC 3.0.