MORE JUICE NEEDED: THE COMING PUSH FOR ELECTRIC POWER

US Electric demand could be on the verge of a structural acceleration driven by the intense power needs of a digitized and electrified world. After a decade of flat growth, many US electric utilities and the North American Electric Reliability Council (NERC) are raising previous forecasts to reflect stronger sales growth driven by the growing use of power hungry technology (artificial intelligence), data centers, electrification, reshoring of manufacturing, and bitcoin mining. This report explores the coming balance between demand for electricity due to Artificial Intelligence (AI) and Electric Vehicle (EV) demand, along with identifying participants within the electric ecosystem that may benefit from this dynamic.

- A December 2023 report “The Era of Flat Power Demand is Over” by Grid Strategies, grid planners (regional transmission organization – RTO) that coordinate the movement of wholesale electricity, nearly doubled the 5-year load growth forecast over the past year. The US forecast of electricity demand growth rose from a cumulative 2.6% to 4.7% over the next five years. According to Boston Consulting Group, the data-center share of U.S. electricity consumption is expected to triple from 2022 by 2030 (equal to 40 million U.S. homes). McKinsey sees data center demand CAGR of 15% over 2023-2030, which translates to 400 TWhs (60 GWs) or 8% of all U.S. power demand– up from 4% today.

- Technology and AI are advancing in real-time and the US power network (generation, distribution and transmission) has been “caught somewhat off guard.” The supply demand situation was already causing concern due to the ongoing retirement of baseload coal and replacement with intermittent wind and solar. NERC’s Annual Long-Term Reliability Assessment-December 2023 raised some concern that rising peak demand and the planned retirement of 83 GW of fossil fuel and nuclear generation creates reliability blackout risks for portions of the US. A surplus demand would likely strain an aging electric network resulting in higher power prices and some regional power supply shortages.

- To meet expectations, the electric utility sector needs significant infrastructure investment. The dynamics create a long-term favorable environment for electric utilities, non-regulated power players, electric infrastructure builders and equipment suppliers. Growing load benefits regulated utilities as it leads to EPS growth through sales growth, rate base growth and improves affordability.

- In non-regulated power markets, which is primarily Texas, New England, and the Northeast, a handful of merchant power companies (CEG, NRG, VST) benefit from selling power at higher market prices. Hyperscalers (Amazon, Meta, Alphabet) require reliable (24/7/365) power and prefer zero-carbon generation (wind/solar/battery storage). As a result, renewable developers (AES, NEE) have substantial opportunity to add wind, solar and battery storage and at enhanced margins. Finally, the build out of the transmission and distribution network leads to growing demand for electrical equipment suppliers (HUBB, VMI) and contractors to install (MYRG, PWR).

EXPLOSION OF AI and EVs

CAN THE GRID HANDLE IT?

After A Decade of Flat Growth, Electric Demand Growth Could Accelerate

According to the US Energy Information Administration (EIA), US electric demand grew a modest 5% over the past 10 years (2013-22 was 5.4%). EIA’s March 2024 Short-Term Energy Report forecasts 2% growth in 2024 and 1% in 2025 after falling by 2% in 2023 due to mild weather. From 2024 to 2026, International Energy Association (IEA) has a similar forecast with US electricity demand growth of 1.5% per annum due to increased manufacturing activity and electrification in the transportation and building sectors. Around one-third of the additional demand is expected to come from data centers. However, these government agency numbers could prove conservative.

According to Grid Strategies, the US forecast of electricity demand is likely underestimated and highlights that recent year-over-year 5-year forecasts rose from a cumulative 2.6% to 4.7% growth (2023 FERC filings) with the more recent cumulative forecast for demand growth of 38 gigawatts (GW) through 2028. Since 2023 FERC load forecast filings, several major utilities have further increased near-term electricity demand forecasts. The main drivers are investment in new manufacturing, electrification and data center facilities. Data center growth is the surprisingly strong variable with more aggressive power and infrastructure needs and time-frames. Below we outline the demand drivers.

- Data centers are increasing in number, size, and power intensity. Rising internet usage, videos, 3-D imaging and implementation of artificial intelligence (AI) is forcing technology hyperscalers (Amazon, Meta, Alphabet, etc) to develop more, bigger and more power intense data centers. McKinsey sees data center demand CAGR of 15% over 2023-2030, which translates to 400 TWhs (60 GWs) or 8% of all U.S. power demand– up from 4% today. Over the past six-months, many electric utilities (SO, WEC, ETR, BKH) have raised electric demand forecasts to reflect the additions of large data center loads.

- New manufacturing facilities (computer chips, batteries). US manufacturing on-shoring is aided by incentives under the IRA and CHIPS Act. Some recent examples include a March 2024 Intel announcement of $8.5 billion in Chips Act funding to build fabs in Arizona, New Mexico, Ohio, and Oregon. Other chip manufacturers are also adding fabs. Entergy (ETR), which serves much of the Gulf Coast forecasts 6-7% industrial sales growth 2022-2026 (16% cumulative) driven by petrochemicals, refining, industrial gases, chemicals as well as data centers, and IRA/clean energy transition.

- Electrification. The public policy movement to replace technologies or processes that use fossil fuels (gas furnaces, boilers, internal combustion engines) with electrically-powered equivalents, such as electric vehicles (EVs) or heat pumps, will drive higher electric demand in some regions. The New England grid operator (ISO) expects heating electrification to turn the regional grid into a winter-peaking system sometime in the mid-2030s. EEI forecasts electric vehicle (EV) adoption to grow from 3 million EVs today to 26 million by 2030, creating a need for 140,000 EV fast charging ports, which would boost load by 1% annually. As the number of EVs on the road increases, grid capacity needs to be expanded to meet the resulting incremental energy demands.

McKinsey and Company forecasts that global power consumption will triple by 2050, natural gas demand will increase 10% in the next decade, and renewable sources will account for 85% of global power generation by 2050. We have highlighted recent examples of larger electric utilities raising forecasts.

- Dominion Energy’s Virginia Power serves the nation’s largest datacenter market in northern Virginia and electricity demand from datacenters grew 500% to 2,700 MWs from 2013 to 2022. PJM (RTO-in 13 Northeast/MidAtlantic states) raised its forecast for summer peaks to 5.5% annually over the next 10 years. Dominion expects to add $2.5 billion of projects to support data center growth.

- In February 2024, Southern Co. (GA, AL, MS) raised its 2025-2028 annual electric sales forecast to 6%, including Georgia Power’s to 9%, (previous forecast was 0-1%) with datacenters driving ~80% of the emerging load growth. The company raised its five-year capital plan by $5 billion to meet growth.

- In 2023, American Electric Power saw its OH commercial sales grow 7.8% in 2023 primarily dominated by datacenters and has “robust” commitments for 2025.

- In November 2023, WEC Energy Group raised its 2024-26 annual electric demand growth forecast to 4.5-5.0%, from 0.7%, to reflect data center and technology demand. Microsoft plans a $1 billion data center near Milwaukee on a science/technology hub developed in collaboration with Foxconn.

- Entergy (ETR) ETR forecasts 6-7% annual industrial sales growth 2022-2026 driven by Gulf Coast industries (petrochemicals, refining, industrial gases, chemicals), and data centers.

ARTIFICIAL INTELLIGENCE 101

The two parts of AI are training (learning the data) and inferencing (applying the data). AI training is when existing datasets are fed into an AI model and learns from the data such as what a cat looks like. AI training is more energy and compute intensive, but more upfront intensive, while AI inferencing is ongoing power intensive. Generative AI, such as ChatGPT, uses inferencing.

For energy, we can infer that AI training is like an initial “investment” cost while AI-inferencing is the continual cost of running AI workloads. Because AI inferencing is a continual energy consumption, much of the energy consumption in the future will be on inferencing. Jensen Huang, founder and CEO of Nvidia, stated that half of Nvidia Graphic Processing Units (GPUs) are currently used for inferencing, and we expect a bigger portion of the GPUs to be used for inferencing as generative AI becomes more ubiquitous with more advanced use cases. At the end of the day, AI models will generate significantly more revenues from AI inferencing than AI training.

During Nvidia’s GPU Technology Conference this year, the company stated that training Open-AI’s latest state of the art AI Large Language Model (LLM) takes about 8,000 Nvidia Graphics’ GPUs and consumes 15MW in 90 days. GPUs are the most energy intensive and important component of AI data centers. GPUs are specialized processors that can compute mathematical equations at high speed. The good news is that the new iteration of Nvidia GPUs will be more power efficient and can do the same AI training task with less energy consumption. For example, Nvidia’s next generation GPUs can train the same Open-AI model for only 4MW in 90 days but this energy efficiency may be offset by increasing computations needed per AI model.

Generative AI functions take up more energy than traditional AI functions. For context, traditional AI outputs specific answers/functions while generative AI generates something new in response to an input. According to research paper by Alexandra Luccioni, Yacine Jernite, and Emma Strubell, generative text-based queries (Generative AI) are about ~23x more energy intensive than text classification queries (Traditional AI). On top of that image generation is 60x more energy intensive than text generation queries. Recently, OpenAI developed text to video capabilities via OpenAI Sora, which is essentially generating 30-60 images per second; one generated minute video can therefore generate 1800 images per minute.

Traditional data center servers (CPU or storage servers) typically consume around 1kW while an AI server like Nvidia DGX H100 which has 8 Nvidia H100 GPUs use ~10.2kW. In an AI server, the most energy and compute intensive part is obviously the GPUs. The current gen AI GPU by Nvidia is the H100 GPU which has max power of around 700 watts. Therefore, in an AI server around 5.6kW is from the GPUs themselves and the rest of the 4.6 kW comes from the CPU, memory, networking, storage, and other systems within the server. Although it is hard to guess how many servers are in each data center, we can reasonably assume for a hyperscaler the server count is at least 10,000 servers within one data center thus around 80,000 GPUs. For context, Mark Zuckerberg has publicly stated that he wants to use 600,000 GPUs to support Meta’s generative AI ambitions.

DATA CENTERS AND THE DIGITAL ECONOMY

OPPORTUNITIES IN INNOVATION

From 2022-2024, the number of US located data centers is expected to grow from roughly 2,700 to roughly 5,400 (McKinsey). By the end of this decade, McKinsey projects that data centers will consume more than 32 GWs of electricity, up from 16 GWs in 2022. Global data generation is rising dramatically propelled by advancements in cloud computing and artificial intelligence (AI). Data centers store data needed for computations and are one of the more energy intense building types consuming 10-50X the energy per floor space of the average commercial building. The power is needed to operate servers, equipment and cooling systems. Hyperscalers provide computing and storage at enterprise scale and need more, larger and more computing intense data centers. Further, they are moving rapidly to secure first mover advantages in locating, siting and building new data centers. We have listed the hyperscalers below:

- Cloud Service Providers (CSPs): Amazon Web Services, Microsoft Azure, Google Cloud, Oracle

- Social Networking Platforms: Meta Platforms, TikTok

- Network Service Providers: AT&T, Verizon, Zayo, Cogent Communications

- Media and Content Companies: Netflix, Disney, Warner Bros Discovery, Activision Blizzard

- Software-as-a-Service (SaaS) Providers: Salesforce, Adobe, SAP, ServiceNow

- Managed Service Providers (MSPs): Rackspace, Dell, Kyndryl, Hewlett Packard Enterprise (HPE)

- Large Enterprises: Walmart, J.P. Morgan, McDonald’s, Exxon, UnitedHealth

Further, AI computing requires more intense use of general processing units (GPUs) versus central processing units (CPUs). GPUs use 3-4X (700-watts versus 200-watts) as much power and are increasing in complexity and intensity. According to Gartner, most AI GPUs will draw 1,000 watts of electricity by 2026, up from the roughly 650 watts on average today. AI will lead to increased data center rack power capacity (up to 50 kW – 100 kW vs less than 10 kW) and require a shift from air cooling to liquid cooling.

In a data center, IEA estimates that 40% of energy requirements come from computing needs, 40% from cooling requirements, and the rest from other IT equipment.

WHO IS THE “COOLEST?” – Exploring Data Center Cooling Providers

The immense amount of heat created by computers within data centers provides a great challenge for hyperscalers and collocating companies to keep temperatures in the 75 degree Fahrenheit range with appropriate levels of humidity. Air flow management is critical to ensure safe usage of equipment. This includes handling hot air expelled from IT equipment that must be appropriately handled to ensure “rack efficiency.” We list two providers of data center cooling equipment below that have already seen massive demand for their cooling solutions.

Data Center Equipment/Cooling Suppliers

There are a host of companies, primarily suppliers of electrical products, who have built up sizable capabilities providing equipment for data centers, notably hyperscalers. While the hottest and fastest growth product category for data centers is thermal management, particularly liquid cooling, power distribution is also experiencing rapid growth. Electrical companies have been rushing to increase their exposure to data centers and invest in incremental capacity. Companies with robust liquid cooling offerings are seeing the strongest demand growth, while companies heretofore light in liquid cooling are investing to catch up.

Vertiv, the data center “pure play,” has leveraged its broad portfolio in thermal management to gain traction in liquid cooling, despite not being as early to nextgen liquid cooling technology. According to Vertiv, AI servers generate five times more heat than traditional CPU servers and require ten times more cooling per square foot. Vertiv sees direct-to-chip liquid cooling remaining the mainstream liquid cooling solution for some time. Here a cold plate made of highly conducive material such as copper is attached to the server’s heat-generating components, inclusive of tubes through which a coolant, typically water, flows. The coolant absorbs heat from the components as it passes through the chamber, cooling those components down, and then is then either expelled or cooled by an external heat exchanger. Air cooling is used for the rest of the components that are not directly exposed to water cooling.

Leaders in immersion cooling are hoping to facilitate a quicker transition from direct-to-chip technology. In immersion cooling, the IT hardware is submerged in a specially formulated dielectric coolant that transfers heat directly from the components. A pump circulates the dielectric fluid within the tank, extracting heat from the servers. The heated fluid then passes through a heat exchanger, where it is cooled by water. This approach maximizes the thermal transfer properties of liquid and is the most energy-efficient form of liquid cooling on the market.

For existing data centers being retrofitted, there are also rear-door heat exchangers, which replace the rear door of the IT equipment rack with a liquid heat exchanger. These systems can be used in conjunction with air-cooling systems to cool environment with mixed rack densities.

Of course, data centers require various types of equipment beyond cooling and thermal management. Power distribution is another key function; data centers receive power from the utility grid at a high voltage level and then distribute it to the IT equipment at a lower voltage. Power distribution includes power distribution units, which manage, convey, and regulate power distribution to IT equipment, remote power panels, which deliver power to the PDUs, as well as switchers, transformers, and uninterruptible power supply. Beyond power distribution are other large product categories like racks, enclosures, connectivity/cabling, and data center software. Table 3 shows the major data center equipment suppliers.

Vertiv Holdings (VRT – $80.00 – NYSE)

Based in Cleveland, Vertiv (VRT – NYSE) is the closest company to a data center pure play, with 75% of sales into data centers, alongside exposure to communications networks and commercial & industrial. Vertiv originated as Emerson network power, was sold to Platinum Equity in 2016 for $4 billion, and was taken public via SPAC by Platinum Equity in February 2020, at which point former Honeywell CEO David Cote joined as Chairman. Vertiv has exposure across a broad set of industrial products supplied to data centers and across geographies, with a leading position in data center thermal management as well as large UPS and Power Switching & Distribution. It does not participate as broadly in electrical offerings. Vertiv also generates over 20% of sales from services & spares. Led by AI and data center demand, Vertiv is expected to grow organic revenue by over 15% between 2022 and 2024, while lifting EBITDA margins from 13% to 19%., with expected 10% top-line growth thereafter.

Modine (MOD – $91.17 – NYSE)

Racine, WI – based Modine (MOD – NYSE) provides an excellent example of a company that has adapted to where the proverbial “puck” was going, positioning itself as a leading provider of cooling equipment for data centers. The company, which traces its roots back to car radiators, has expanded its Data Center business globally, supplying high efficiency air conditioning, IT cooling systems, chillers, condensers, and air handling units for data center usage. In its most recent quarter, Modine called out expectations for Data Center cooling sales growth in the 60 to 70% range. Additionally, the company recently announced the acquisition of Scott Springfield Manufacturing, a Calgary-based manufacturing of Air Handling Units (AHUs) for hyperscale and colocation data centers, adding evaporation-based cooling to its suite of technologies.

Environmental Impact

The environmental impact of data centers is not limited to power consumption. They also have a negative environmental impact due to their water usage, carbon footprint, and waste production.

As of 2024, data centers contribute about 2.5-3.7% of global greenhouse gases (GHG), which is greater than airlines (2.4%). Cloud storage alone produces about 0.2 tons of CO2per 100 GB of data stored in the cloud. Other pollution by data centers includes refrigerants like CFCs and Freon, which are used for cooling and contribute to ozone depletion; diesel, which is used as backup for electricity production; and natural gas, which is used for heating and fueling cells.

Water consumption is an enormous environmental harm of data centers. Data centers use about 3-5 million gallons of water per day to cool the servers, which is enough water for over 30,000 people. Many data centers are in areas subject to drought, such as Dallas and the Bay Area.

Finally, data centers affect the environment through their production of waste. Hardware production, transport, and disposal at end of life all contribute to significant waste. Servers have a relatively short lifespan, requiring replacement every 3-5 years. Electronic waste (E-Waste) is toxic and a significant environmental hazard that impacts air, water, and soil quality, contaminating these compartments with heavy metals and other chemicals.

Data centers can improve their environmental impact through some of the following efficiencies:

- Investing in newer equipment that requires less energy to operate.

- Source their energy from renewables (e.g. installing wind turbines or solar panels, potentially also nuclear power)

- Use cooling techniques like outside water and air that don’t produce emissions.

- Turn off inactive servers, saving about 10-15% of energy.

- Locating new data centers in areas that do not rely on coal for energy.

Large technology companies like Microsoft (MSFT), Google (GOOG), Apple (AAPL), and Amazon (AMZN) have a significant environmental footprint. Due to their enormous projected growth, they are under increasing scrutiny for how they plan to manage their impact on the environment and climate. On a total basis, Samsung has the largest carbon footprint with 20 million metric tons of CO2e per year. Per employee, semiconductor company TSMC emits the most at 209 metric tons of CO2e per year. Many of these tech companies have vowed to reduce their fossil fuel consumption and impact on the environment, some such as Amazon pledging to reach net-zero carbon emissions by 2040 and targeting 100% renewable energy sources by 2025. Their climate initiatives often involve reduction of GHG emissions by using renewable energy. Some companies have proposed the use of nuclear power to achieve this.

In addition to decarbonization, big tech companies have been focusing on supply chain management through efforts that reduce the carbon footprint of the complete lifecycle including supply. Reduction of electronic waste efforts involve recycling of electronics components and focusing on a circular economy, which allows end-of-life products to be circulated back into the economy through buying back products. All these initiatives must be scaled up rapidly to meet the exponential demand forecasted in this sector

ELECTRIC VEHICLE GROWTH…STILL ON THE WAY

Despite near term headlines discussing the current lull in demand for electric vehicles in the United States, we regard the electrification of the 290 million vehicles in the US as inevitable eventuality for which the electric grid must prepare.

We expect annual electric vehicle sales in the US to grow from just over 1.4 million units (including both Battery Electric Vehicles (BEV) and Plug-In Hybrid Vehicles (PHEV)) to over 4.5 million units by 2030. Cumulative EVs in operations, also known as the EV vehicle parc, is expected to grow from just under 3 million units at the end of 2022 to over 25.2 million by the end of the decade – still less than 10% of the overall vehicle population but massive growth nonetheless.

Table 4 (below) summarizes growth in both BEV and PHEV sales over through the 2020s.

This growth in electric vehicle adoption will be driven by several factors:

- The elimination of range anxiety. While over 80% of electric charging is expected to be done at home, consumers still have expressed concerns that a lack of availability of public charging stations render them less excited to purchase an electric vehicle for the first time.

- New, affordable SUV and CUV models. Recently, EV adoption has been most notable in SUV and Crossover models that more closely resemble the overall population of the current US fleet. Coming models such as the Chevy Equinox EV (next page) are set to be well received by consumers desiring EV models at price points more similar to the Internal Combustion Engines models they currently drive.

Charging Station Build out set to explode

The pace of EV adoption will largely hinge not only on vehicle model proliferation, but also massive investment in growth in charging infrastructure. Globally, EV Charging Station company Wallbox sees the need for upwards of 100 million chargepoints (at over 12.5 million charging stations) installed for passenger electric vehicles by 2030, a 10x ramp from what will likely be near 10 million by the end of 2022. Similarly, Blink Charging (BLNK), expects annual US EV Charger sales to increase from roughly 500,000 chargers in 2021 to 1.8 million by 2030, with the total number of charger sales over the next decade to add up to just shy of ten million chargers.

Charging solutions are likely to take several forms, with Home and Business Charging systems in the 7-22 kW range (according to Wallbox, over 70% of all charging occurs at home and work) the overwhelmingly greatest need. Public Charging stations utilizing Level 2 (60-150kW) chargers will likely constitute the next greatest set of charging equipment needs, while “superfast” 150-400kW Public DC fast chargers will likely find some level of demand for highway driving and/or other specialized cases.

Charging companies have sought to work together with public utilities on “bi-directional” charging that provide opportunities to integrate renewable energy, battery storage (via the vehicle itself) and the broader electrical grid. The opportunity to reduce energy costs, reduce dependency and stress on the grid, along with the potential for carbon emission reduction all combine to increase the opportunity that exists within the charging space.

MEETING THE DEMAND – HOW ELECTRIC POWER PROVIDERS BENEFIT

Over the near-term, the tech sector’s power appetite could prove too much for the realities of the slower moving power network. US power demand was already forecast to increase at a 1% CAGR due to EVs & re-shoring of manufacturing (vs flat historically) with expected tight conditions due to the great power transformation from coal to renewables. According to NERC’s Annual Long-Term Reliability Assessment-December 2023, the Northeast and Western half of the U.S. face an elevated risk of blackouts in extreme weather conditions and parts of the Midwest and central South areas could see power supply shortfalls during normal peak operations. To address the growing risk, NERC recommends new gas capacity and transmission investment.

Hyperscale data center players need power and value reliability, clean energy (wind/solar/battery storage) and speed to market over price. They require 24/7/365 power meaning a dedicated power source, grid connections, and grid redundancies while meeting ESG carbon standards. Nuclear power generation can deliver 24/7/365 reliability with zero carbon emissions and has suddenly become highly valuable. In addition, the Inflation Reduction Act (IRA) provided inflation-adjusted tax credits to ensure nuclear plants did not retire.

US electric utilities and power generators will benefit from selling existing power capacity, adding power capacity (including batteries) and upgrading/expanding the transmission and distribution network trying to keep up. Surplus demand growth enhances regulated electric utilities ability to deliver mid-single digit EPS growth. Further, spreading costs over a larger sales base improves affordability. Favorable areas for data centers are near strong transmission and fiber networks, including northern VA, Silicon Valley CA, Dallas, TX. Although most electric utilities benefit from the network buildout and enhanced rate base growth.

Capital Investment (Rate Base) Continues to Rise and Drive Healthy Earnings Growth

In 2023, EEI member electric utilities invested an estimated $167.8 billion, which marks the eleventh consecutive year of record investment. This compares to an estimated 2022 record investment of $150.8 billion ($136.6 billion in 2021) in utility infrastructure, including distribution ($51 billion, or 33%), generation ($37 billion, or 24%), transmission ($32 billion, or 20%), gas-related ($22 billion, or 14%) and other ($13 billion, or 8%). Over the next several years, utility capital investment will continue to rise.

- Clean energy transformation (coal retirements, on/off-shore wind, solar, and storage).

- Electric transmission and distribution (grid modernization, hardening, undergrounding).

- Electrification, EV charging, efficiency, etc.

COAL AND GAS RETIREMENTS – NOT SO FAST, MY FRIENDS

While hyperscalers want renewable energy, nuclear, coal and gas power are more consistent power generators. In 2023, the US had ~1,200 GWs of power capacity, including 215 GWs of renewables (74 GWs of utility-scale solar (6%) and 141 GWs of wind capacity (12%). Based on the EIA March Short Term Energy Forecast, the power sector added 19 GW of solar capacity in 2023 (27% increase) and is expected to add 36 GW in 2024 and 35 GW in 2025. Gas-fired generation is expected to fall from 42% of

total generation in 2023 to 41% in 2025, while coal generation is expected to fall from 17% in 2023 to 14% by 2025. Nearly 20% of U.S. coal-fired generating capacity has been retired since 2020.

Based on planned retirement schedules, coal’s rapid decline will continue, and all new capacity will be renewable, battery-storage and/or natural gas-fired (excluding the 2.2 GWs Vogtle nuclear expansion scheduled for 2023-24). Over the past decade, less-efficient nuclear (13 retirements since 2013) and gas power plants were retired and replaced with highly efficient natural gas plants and renewable generation.

According to EEI (April 2023), developers plan to add 478 GWs of capacity over 2023-2027, including 228 GWs of solar, 104 GWs of wind, and 101 GWs of storage. With that said, we do not expect that anywhere near as much will come on-line over that time-frame because of permitting, siting, financing, regulatory and other delays. Over the same period, EEI projects 102 GWs of capacity retirements (42 GWs of coal, 40 GWs of gas, and 16 GWs of oil).

THE NUCLEAR OPTION

A Return to Nukes?

Nuclear power generation is the most reliable form of power generation with capacity factors normally over 90% (meaning they run nearly all year long) and have a near zero carbon footprint. The US has 93 nuclear reactors (54 plants) in 28 states that generate roughly 19% of the nation’s power capacity, which compares to 104 nuclear reactors in 2013 and 20% of total US generation. Prior to the 2022 IRA, several older nuclear units retired as low gas prices (and therefore power prices) made them uneconomic. However, the IRA provided a floor price via production tax credit of ~45/MWH and an increased focus on data center/zero carbon power has breathed new life into the future of nuclear power.

The Nuclear Shot Heard Around the World

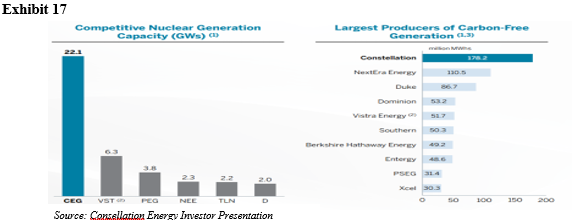

On March 4, 2024, Talen (TLNE-90-OTC) announced a deal to sell its digital infrastructure campus (data center and crypto mining facilities) to Amazon Web Services Inc. for $650 million. The campus is adjacent to its Susquehanna nuclear plant (2,500 MW’s) near Berwick, PA, which allowed TLNE to directly supply 960 MW of zero-carbon power to the data center campus. The deal potentially increases the value of merchant power plants (especially nuclear) as hyperscalers are less price elastic and could contract directly. There are roughly 40 GW’s of non-regulated nuclear power plants owned by CEG, VST, PEG, NEE, TLN and D that can benefit from the power surge.

These strong attributes (zero-carbon, reliable, economies of scale) augur for building more nuclear plants, especially given the pending surge in demand for zero carbon power. However, the challenges of building new nuclear capacity are significant and there have only been two nuclear units built in US over the past 40-years. Southern Company’s Georgia Power’s Vogltle Units 3 and 4 (2023 and 2024) were the first new nuclear units to come online in the U.S. since Palo Verde (AZ) in the 1980s (TVA’s Watts Bar – 2016 excluded). Approvals from the Nuclear Regulatory Commission (NRC), permitting, planning, and construction takes several years and the costs often underestimated. Vogtle Units 3 &4 were originally scheduled to be completed by 2016 and 2017, respectively, at a cost of $14 billion total. However, the final price tag was $30 billion, more than $16 billion over budget, and over six years behind schedule.

Small Nuclear Reactors Could Be the Power of the Future

The US probably will not add a large sale nuclear plant for some time, but existing nuclear plants will seek license extensions and some recently retired plants could return to service. Further, the appetite for zero carbon power increases the likelihood that small nuclear reactors (SMR’s-300-MW‘s) become a reality. To date, the N.R.C. has certified one small reactor design, NuScale Power (SMR), which took a decade and cost $500 million. Below we highlight some entities pursuing SMR’s:

- NuScale Power Corporation (SMR) (Portland, OR) SMR is a developer of a small pressurized water reactor that can each generate 77 –MW’s and scaled in an array up to 924 MWe (12 modules). In January 2024, NuScale’s first pending project was canceled due to escalating costs ($5.3 billion to $9.3 billion). Standard Power, a provider of infrastructure as a service to data centers is working with NuScale Power to develop SMR-powered facilities in Pennsylvania and Ohio.

- Terra Power (Bill Gates, founder, funder and Chair) hopes to submit an NRC construction permit in 2024. The advanced nuclear reactor and energy storage system will be sited near a retiring coal facility in Wyoming. The Natrium reactor demonstration project is a public-private partnership, and part of the U.S. DOE’s Advanced Reactor Demonstration Program (ARDP) and features a 345MW sodium-cooled fast reactor with a molten salt-based energy storage system. The storage technology can boost the system’s output to 500MW (400,000 homes). The project’s target a 2030 operation date.

- Holtec International, which specializes in nuclear storage and decommissioning, intends to license and construct two SMR-300 units by mid-2030. Holtec owns the Michigan Palisades nuclear plant (retired in May of 2022; originally owned by CMS Energy and sold to Entergy in 2007) plans two new small modular reactors on site. Holtec intends to license and construct two SMR-300 units by the mid-2030s. Each new pressurized water reactor will be able to produce 300-MW’s to the 800-MW plant. Holtec is aiming to restart the plant by the end of 2025. Holtec plans to file a construction permit application to the NRC by 2026.

- GE/Hitachi (GEH) developed a BWRX-300, an advanced reactor using the natural circulation and passive cooling isolation condenser systems. GEH believes the BWRX can be constructed in 24-36 months reducing the building volume and concrete size. GEH has a US NRC permit for the Tennessee Valley Authority (TVA) at the Clinch River site in Oak Ridge, TN. (the only site permit in the US). In addition, Ontario Power Generation selected GEH BWRX-300 for the Darlington New Nuclear Project. Construction could be complete by late 2028.

- X-Energy, a start-up in Maryland, is developing a pebble-bed reactor, and has JV with Dow to develop a four-unit Xe-100 facility at one of Dow’s U.S. Gulf Coast sites. In 2020, the DOE awarded X-energy up to $1.2 billion under the ARDP in federal cost-shared funding. X-energy is preparing to submit an application for licensure to the NRC.

Finally, clean hydrogen production, which involves the electrolytic generation of hydrogen gas from water using clean energy sources including nuclear power, is poised to receive $8 billion from the Bipartisan Infrastructure Law to demonstrate regional clean hydrogen hubs including at least one using nuclear. Hydrogen gas is expected to be an important part of the future global energy economy.

First Wave of Beneficiaries

Independent Power Producers (IPPs), also known as merchant generators, are the most leveraged beneficiaries to supply shortages. IPPs/merchants own power plants in non-regulated power markets, including PJM (Northeast/MidAtlantic), ERCOT (Electric Reliability Council of Texas), and California, and provide marketing or power management services to customers. Constellation Energy (CEG) and Vistra Corp (VST), highlighted below, are the most leveraged to higher power prices, followed by NRG Energy (NRG) and Talen Energy (TLNE) discussed in appendix. IPPs and merchant power companies are higher risk companies than utility stocks and earnings are highly correlated to commodity prices.

Constellation Energy (CEG – $190.26 – NYSE)

Based in Chicago, IL, Constellation Energy (CEG – NYSE) is an independent power company spun-off from Exelon (EXC- $55 – NYSE) in February of 2022. CEG owns 32,000 MW’s of capacity, including the nation’s largest nuclear fleet totaling 21,000 MWs of nuclear (12 nuclear stations and 21 reactors) primarily in the PJM markets, including IL (55%), Mid-Atlantic (MD and PA-30%) and New York (15%), 6,000 MW of natural gas and 3.6 GWs hydro, wind and solar. The company’s retail marketing segment provides energy products and services to largely commercial and industrial (C&I) customers. With IRA tax credits as a floor, CEG no longer needs to enter into long-term contracts and benefits from rising power prices. In November 2023, CEG completed the acquisition 44% ownership stake in the South Texas Project Electric Nuclear Plant (STP), a 2,645-MW, dual-unit near Houston, TX, from NRG. Price implied 11.7x EV/EBITDA.

Vistra Energy (VST – $73.76- NYSE)

Based in Houston, TX Vistra Energy (VST – NYSE) is a power generation and energy marketer. In 2016, Texas Competitive Electric Holdings (TCEH), parent company of TXU Energy and Luminant, emerged from Chapter 11 (as part of the bankruptcy protection for Energy Future Holdings Corporation). TCEH was rebranded as Vistra Energy. In 2018, Vistra Energy and Dynegy merged. VST’s power portfolio totals 37,000 MW of generation capacity, including 18.9 GW’s in Texas (2.4 GWs nuclear; 4.6 GW’s coal; 0.45 GWs solar; 12 GWs gas), the East PJM/ISO-NE (12 GWs gas; 0.1 GWs oil), 1.9 GWs in California. The company owns 3,750 MW of zero-carbon generation, including 2,400

MW of nuclear generation at Comanche Peak facilities. In late March 2024, VST closed on the acquisition of Energy Harbor’s nuclear (~4 GW) and retail businesses (~1 million customers). Energy Harbor owns the Beaver Valley 1 and 2, Perry, and Davis Besse nuclear plants and retail businesses. VST’s 2024 Adjusted EBITDA guidance is $3.7-4.1 billion (Energy harbor to add $700-900 million).

Long-term Wave of Beneficiaries

Tighter power markets, increasing renewable portfolio standards and growing demand specifically for clean power makes for a very favorable renewable development market. NextEra Energy (NEE) is the largest renewable owner, operator and developer in the US with the largest development pipeline. Other large owners, include AES Corp, Berkshire Energy, Brookfield, and Iberdrola/Avangrid and privately-held developers Invenergy (private), Apex (private) and Hecate (private). Over next seven years, NEE believes the US needs 375-450 GWs of renewables (wind/solar/battery storage) compared to 140 MWs added over last seven. The US currently has roughly 1,200 GWs of total generating capacity.

Large corporations and hyperscalers want to secure clean energy contracts primarily to meet internal ESG goals. According to S&P Global Commodity Insights, US tech corporations have signed 57.7 GW of renewable energy capacity, including Amazon (28 GW), Platforms (10.5 GW), Alphabet Inc. (9.5 GW). From February 2023-February 2024, nearly 20 GWs of renewable capacity (70% solar) was signed in more than 200 deals to corporate buyers, primarily the tech industry.

As noted earlier, renewable developers have aggressive plans but face long waiting lists (often 3-7 years) to interconnect to the grid. The transmission system was not designed to handle massive renewable additions, particularly given wind/solar intermittency. The ability to site new renewables is key to successful development, which entails not only finding locations where the wind/sun resources are strong, but near transmission/substation interconnections, water, fiber and a constructive local planning council. NEE and AES highlight competitive advantages of scale, experience and access to technology as well as site locations,

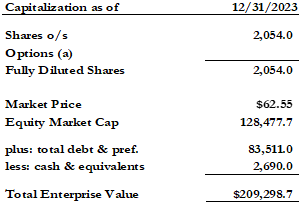

NextEra Energy (NEE – $62.55 – NYSE)

Based in Juno Beach, FL, NextEra Energy’s (NEE – NYSE) primary subsidiary, Florida Power & Light (FP&L), is the largest electric utility in FL, and NextEra Energy Resources (NER), is a leading wholesale power generator. FP&L serves 5.8 million customers in Eastern, Southern and Central-Western Florida (34 GWs of generation; 73% gas; 14% nuclear; 14% other). NER owns 34 GWs of net non-regulated generation (23-GWs wind; 6 GWs solar; 2 GWs nuclear; 3 GWs batteries), including the nation’s largest wind portfolio. NEE owns 101.4 million common units (~58%) of NextEra Energy Partners (NEP-30) NER plans to grow its non-regulated renewable portfolio to 63 GWs by 2026 (backlog includes 6 GW of AI data centers) and has a development pipeline of 300 MWs. NEE has ready-to-go renewable sites with interconnection and transformers needed through at least 2027. NEE sees itself keeping 20% market share or better and 500-1000 bps of incremental return achieved which supports their 20%+ targeted levered returns on wind/storage and mid-teens on solar. NEE has and can provide clean/reliable solutions that include wind, solar, storage, and select grid purchases and RECs.

AES (AES – $17.90 – NYSE)

(Arlington, VA) AES (AES – NYSE) is a global energy company with four segments: US and Utilities (U.S., Puerto Rico & El Salvador); South America (Chile, Colombia, Argentina & Brazil); MCAC (Mexico, Central America & the Caribbean); and Eurasia (Europe & Asia). As of 2023, AES owned 34.6 GW’s (24 GWs net) of generation (53% renewable, 18% coal, 27% gas,). AES’ six utility businesses distribute power to 2.6 million people, including Indianapolis Power & Light ($3.4 billion rate base/4,100 MW) and Dayton Power Light ($784 million) utilities in El Salvador. ADJ Pre-Tac Contribution: 41% US and utilities; 27% South America; 20% MCAC; 12% Eurasia. AES owns 35% of Fluence (FLNC-17) commercial and industrial battery storage. In 2023, AES signed long-term contracts for 5.6 GW of renewables, bringing its project backlog to 12.3 GW. AES recently contracted all of its 1,000 MW planned Bellefield 1&2 solar projects (500-MW’s; 2025-26) in CA to Amazon. AES also has long-term contracts to supply carbon-free power to Microsoft Corp. datacenters in California and Google datacenters in VA.

All Electric Utilities Benefit Upgrading the Power Grid for Renewables and Demand

The significant increase in data centers and renewable power generation creates demands on the transmission grid. Even if new power generation is situated near new data center clusters, such clusters will strive to be served by at least two transmission lines, allowing for redundancy in the event of grid problems. This will likely require the build out of new transmission lines. As importantly, data centers should accelerate the modernization and hardening of the transmission and distribution grid because of their intensive power demand. New transformers, insulators, connectors, and enclosures will be in demand. And the companies producing these products should benefit not only from increased demand but also from improved pricing and operating leverage.

Electric utilities are allocating a growing amount of capital resources on power grid adaptation, hardening, and resilience (AHR) initiatives. According to the DOE, almost 70% of electric infrastructure in North America is over 25 years old. AHR is increasingly becoming an important way that electric companies fulfill their mission of supplying clean, reliable, and affordable energy to customers. In 2023, EEI member utilities invested $57 billion in electric distribution and $30.7 billion in electric transmission compared with $51.3 billion and $31.7 billion in 2022. A number of utilities implement system upgrades and hardening programs in response to recurring severe weather events to make their systems more resilient to hurricanes and wildfires. Underground transmission and distribution initiatives in California, northeast coastlines support increasing demand for energy, including those from intermittent renewable sources.

Over the next few years, we expect FERC to solidify numerous policy directives and incentives, including ROE methodology, transmission planning and the interconnect process, as well as the need to alleviate the clean energy logjam, and gas pipelines. The nation’s RTOs are highlighting concerns and requesting investment. The Midwest Independent System Operator (MISO) approved Tranche 1 of its $100 billion long-term planning projects, and awarded (2022) 18 transmission projects, totaling $10.3 billion and spanning IA, IL, IN, MI, MN, MO and WI. Winning bidders, included: Ameren (AEE) – $1.7-1.8 billion, Xcel Energy (XEL) – $1-2 billion, Fortis (FTS) – $1.0-1.5 billion, WEC Energy Group (WEC) – $800 million.

The projects are expected to be in-service in 2028 – 2030. LRTP projects are significant because they will help accommodate the influx of renewables needed to meet state and utility clean energy goals. We expect Tranche 2 to be awarded in late 2024. The ISO New England electric grid expects $1 billion in annual transmission investments through 2050 to support the clean energy transition, and could still face potential resource adequacy challenges. ISO-NE expects gas generation to fall from about 45% of New England’s electricity production in 2022 to about 12% in 2040 and renewables will rise from about 11% to 56% across the same period. Batteries will play a key role in the future power supply dynamics. As an example, the NE-ISO is attempting to integrate 40 GW of resources in the ISO’s interconnection queue, 46% of which are battery storage.

Grid Beneficiaries – Power Generation Buildout

The AI play will be more in transmission than in distribution, and more on the electrical side than the mechanical side. Over the last ten years, utility distribution capex increased at an ~10% CAGR to $57B driven by grid hardening and modernization to address wildfire and storm concerns, while transmission capex still grew at a healthy 5% CAGR.. Data centers may begin to tip the growth balance in favor of transmission, with Hubbell projecting high-single digit end market growth in 2024 in electric transmission & substation and mid-single growth in electric distribution.

Hubbell (HUBB – $424.40 – NYSE)

Based in Shelton, CT, Hubbell (HUBB – NYSE) is the largest US provider of utility transmission & distribution components, with over 25% market share, more than twice that of privately owned MacLean Power Systems. Its relative share versus Eaton and ABB is even larger. Utility T&D components, which is three-quarters of utility solutions segment sales, comprised $2.46B of Hubbell’s $5.37B of sales in 2023 (46%) and perhaps nearly 60% of EBITDA. Nearly 75% of Hubbell utility T&D sales go to electric utilities, of which two-thirds is electric distribution and one-third electric transmission & substation.

Utility T&D components is a high EBITDA margin (likely high 20s), high multiple business responsible for roughly two-thirds of Hubbell’s asset value. Hubbell further strengthened its position during COVID given fewer supply constraints than competitors. Hubbell expects utility T&D market growth to continue growing at a mid-single digit pace, reflecting grid modernization and expansion, and before considering any meaningful boost from data centers. It also expects to sustain margins in the high-20s, well above pre-COVID levels.

Valmont (VMI – $220.34 – NYSE)

Based in Omaha, NE, Valmont (VMI – NYSE) is the largest provider of utility structures, namely transmission and distribution poles. In 2023, transmission, distribution, and substation comprised $1.24B, or 40% of its infrastructure segment sales, and one-third of company sales. Valmont will benefit from extending the transmission grid to support AI data center clusters, although less than grid component players, who will see upgrade related demand. If renewables can be ramped to support increased power generation for data centers, the grid in turn will need longer transmission connections from areas where the wind blows and the sun shines. Valmont will also continue to benefit from existing secular drivers – 1) grid hardening in distribution, 2) and transmission to support existing renewables projects.

Grid Edge Intelligence

Today’s residential grid is being tasked with charging electric vehicles and other intermittent sources of electricity demand. The challenge is to get more electricity production out of existing generation by spreading out demand during the day, particularly as it relates to EVs and other electricity-heavy appliances. Even when generation capacity is sufficient, transformers at a house, community, or neighborhood level are increasingly testing their load limits. A medium speed electric vehicle charger (i.e. Level 2) operates at 240 volts, consuming as much electricity as a house while that EV is being charged. Air conditioning and laundry machines are other electricity intensive appliances that can strain the system, particularly if competing for electricity with EV charging or relying on intermittent power supply from local solar panels. Grid edge intelligence is mostly a distinct problem from data center needs given limited geographical overlap.

Smoothing out demand is both simple and difficult. Measure electricity consumption super-locally and in real time. Then analyze and share that data with utilities so that they can ensure the grid is not overloaded, causing power outages. Then educate consumers so that they can adjust their electricity consumption when needed, for example by delaying EV charging during peak hours or by running their AC system a bit less hard. This exercise is grid edge intelligence. It starts with networked meters that can measure electric loads hundreds of times a second. It is enhanced by software and data solutions for the utility, and tools that empower customers to adjust their electricity usage when the grid edge is strained. The primary beneficiaries are the dominant electric metering companies – Itron, Landis + Gyr, and Hubbell’s Aclara, although Hubbell is poised to see far more upside from its utility T&D components business.

Itron (ITRI – $89.55 – NASDAQ)

Based in Liberty Lake, WA, Itron (ITRI – NASDAQ) is the largest metering company in the US and worldwide, leading the migration to networked meters, grid edge intelligence, and smart infrastructure. Networked meters comprised 2/3 of the company’s $2.17B of 2023 revenue, with lower technology devices about 20% and the remainder in outcomes sales, leveraging data provided by the networked meters. The outcomes segment is poised for double-digit growth driven by grid edge intelligence and other smart infrastructure such as street lighting. Itron’s technology and solutions were arguably ready to serve grid edge intelligence needs five years ago, although utility demand was slow to materialize. Grids were not as strained in a pre-EV world, demand growth was delayed by COVID, and supply chain challenges on the back end of COVID hindered delivery of backlog.

For Itron’s vision to translate to financial results, it will not only need to encourage utilities to invest behind grid edge intelligence, but also improve its operational performance and drive margins towards its target 15%+ level. The stock’s recent surge following strong Q4 results has left it trading over 25x forward earnings, a valuation that either assumes improved execution or grants Itron a multiple premium with some resemblance to what the likes of Badger Meter enjoy on the water meter side.

Landis+Gyr (LAND – CHF 68.60 – Zurich)

Based in Cham, Switzerland, Landis+Gyr (LAND – EB) is often overlooked by investors compared to Itron because it trades in Zurich, generates close to half its revenue outside of the Americas, and was not as early to introduce networked meters and focus on grid edge intelligence. CEO Werner Lieberherr has established a dynamic culture at Landis, which has allowed it to largely catch up with Itron across its networked meters and software & services offerings, while generating a number of key wins among US electric utilities. Landis is actively driving grid edge intelligence solutions, like Itron, and executing bolt on M&A to expand in smart infrastructure, including EV charging.

Utility Contractors

The dynamics present a long-term runway of opportunity for utility contracting companies like Quanta (PWR), MYR Group (MYRG), MasTec (MTZ) and Primoris (PRIM). Furthermore, the favorable characteristics of natural gas could also position North America as a leading competitor in the global LNG export market, which could provide additional opportunities for utility construction services. As electric utilities undergo multi-billion dollar grid modernization and reliability programs, utility contractors enter into master service agreements.

Quanta Services (PWR- $262.99 – NYSE)

Based in Houston, TX, Quanta Services (PWR – NYSE) is leading provider of infrastructure the electric and gas utility, renewable energy, communications, pipeline and energy industries in the United States, Canada, Australia. provide engineering, procurement, construction, upgrade and repair and maintenance services for electric power transmission and distribution networks; substation facilities; wind and solar generation and transmission and battery storage facilities; communications and cable multi-system operator networks; gas utility systems; pipeline transmission systems and facilities; and downstream industrial facilities.

Appendix (IPP’s, Utilities, Contractors, Suppliers to Benefit From Power Buildout)

Independent Power Producers/Energy Merchants/Utility-Hybrid

NRG Energy (NRG – $72.01 – NYSE)

Based in Princeton, NJ, NRG (NRG – NYSE) is leading energy and home services company. NRG’s strategy is to maximize stakeholder value by being a leader in the emerging convergence of energy and smart automation in the home and business. The company owns 13 GW’s of power plants (5.7 GW’s gas, 6.7 GW’s coal, 0.5 GW’s of oil, and 0.2 GW’s of solar) throughout the US., including TX (8.5 GW’s; 4.2 GW’s of coal), the Northeast (2.5 GW’s), and the West (2.1 GW’s). In March of 2023, NRG bought Vivint Smart Home for power and gas marketing and smart home technology (rooftop solar, HVAC, home security, protections plans). In November 2023, NRG completed the sale of its 44% ownership stake in the South Texas Project (STP), a 2,645-MW, dual-unit near Houston, TX, to CEG for $1.75 billion. 2024 Adj. EBITDA Guidance: $3.30-3.55 billion (Texas-$1.665-1.785; EastWestServices/Other-$810-890 million; Vivint-$825-875 million)

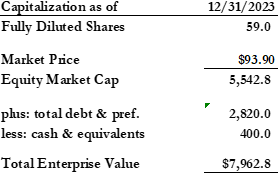

Talen Energy Corporation (TLNE – $93.90 – OTCQX)

Based in Allentown, PA, Talen Energy (TLNE – OTC) emerged from bankruptcy in May 2023 and is PPL Corp’s (PPL) former merchant power business and owner of the Susquehanna nuclear plant (2,500 MW’s). Talen owns and operates 12.4 GW’s of power, including PJM, ERCOT and WECC, Mid-Atlantic, Texas and Montana. 2024 Adjusted EBITDA is $640-840 million

Public Service Electric & Gas (PEG – $63.00 – NYSE)

Based in Newark, NJ, Public Service Electric & Gas (PEG – NYSE) is one of the larger electric and gas utilities in the nation. Public Service Electric and Gas Co. (PSE&G) is New Jersey’s largest provider of electric and natural gas service – serving 2.3 million electric customers and 1.9 million gas customers. PSEG Power owns 3,766 MWs of nuclear (57% of Salem 1&2 for 1,320 MW’s in NJ; 100% of 1,173 MW’s Hope Creek in NJ; 50% owner of Peach Bottom 2&3 for 1,275 MW’s in PA).

Utility Contractors

MYR Group (MYRG -$174.90 – NASDAQ)

Based in Thornton, CO, MYR Group (MYRG – NASDAQ) is leading specialty contractor serving the electric utility infrastructure, commercial and industrial construction markets in the US and Canada. The Transmission and Distribution design, engineer, procure, construct, upgrade and maintain and repair high voltage transmission lines, substations and lower voltage underground and overhead distribution systems, clean energy projects and electric vehicle charging infrastructure. The T&D segment also provides emergency restoration services. Commercial and Industrial segment engages in commercial and industrial wiring, the installation of intelligent transportation systems, roadway lighting, signalization and electric vehicle charging infrastructure for airports, hospitals, data centers, hotels, stadiums, commercial and industrial facilities, clean energy projects, manufacturing plants, processing facilities, water/waste-water treatment facilities, mining facilities, intelligent transportation systems, roadway lighting, signalization and electric vehicle charging infrastructure.

MasTec (MTZ $95.01 – NYSE)

Bases in Coral Gables, FL MasTec (MTZ – NYSE) is a leading infrastructure construction company operating under five operating and reportable segments: (1) Communications; (2) Clean Energy and Infrastructure; (3) Power Delivery; (4) Oil and Gas and (5) Other activities include the engineering, building, installation, maintenance and upgrade of communications, energy, utility and other infrastructure, such as: wireless, wireline/fiber and power delivery infrastructure, including transmission, distribution, clean energy and renewable sources; pipeline infrastructure, including for natural gas, water and carbon capture sequestration pipelines and pipeline integrity services; heavy civil and industrial infrastructure, including roads, bridges and rail; and environmental remediation services.

Equipment Suppliers – Grid and Data Center

Arcosa (ACA – $83.60 – NYSE)

Based in Dallas, TX, Arcosa (ACA – NYSE) is one of the two other major providers of utility structures, along with privately owned Sabre. Given its build out of its construction products businesses (mainly aggregates), utility structure today represents 15-20% of consolidated sales and 10-15% of consolidated EBITDA.

Preformed Line Products (PLPC – $126.57 – NASDAQ)

Based in Mayfield, OH, Preformed Line Products (PLPC – NASDAQ) is a provider of mechanical grid components to utilities, and has a global footprint. In 2023, its USA segment comprised $367mm of $690mm of sales (53%), of which energy (i.e. electrical) was 2/3. We estimate that half the company’s EBITDA was generated from its US electrical business. Mechanical components, like structures, will benefit from an expanded transmission gird to support data centers, although there may be some upgrade demand as well.

Siemens (SIE – €176.54 – Frankfurt )

Based in Munich, Germany, Siemens (SIE – XE) is a German large cap global electrical equipment player with a leading position in Grid Protection and Automation. The relevant Smart Infrastructure segment is approx. 25% of the group and includes power distribution systems, grid design & simulation and management software, micro-grids and charging infrastructure for EVs. Datacenters for Siemens is a $1.3 billion business with approx. $2 billion+ in terms of orders and the company expects 10% annual growth over the medium term. The company is a global leader in software for grid planning & control and sells medium-voltage gas insulated switchgear, microgrids, circuit protection. In addition to low-voltage power distribution products for data centers, Siemens also offers DCIM, HVAC integration, management, security/fire management and energy performance services for buildings including data centers.

nVent Electric plc (NVT – NYSE – $76.00)

With US headquarters in Minneapolis, nVent Electric (NVT – NYSE) designs, manufactures, and services electrical connection and protection products globally. It operates in three segments: Enclosures, Thermal Management, and Electrical & Fastening Solutions. The company spun off from Pentair in 2018 and has been led by former Honeywell executive and Pentair electrical president Beth Wozniak since spinoff. nVent has grown its data solutions business from ~$100 million in sales at the time of spin to $450mm in 2023, mostly organically, with growth in excess of 25% annually from 2020 to 2023. Well over 40% of data solutions sales are in the faster growing areas of cooling and power, although it also offers enclosures, solutions in cable management and leak detection. Less than 10% of data centers are liquid cooled today, and liquid cooling is growing at 3x the rate of legacy cooling, providing a runway for nVent’s continued growth in data centers. nVent has invested to double its liquid cooling capacity, due online late 2024.

ABB (ABBN – Zurich – CHF 41.95)

Based in Zurich, ABB (ABB – EB) is a large Swiss cap global electrical equipment player with exposure to medium-voltage and low voltage (MV) products in data centers. ABB has grown the MV (switchgears, UPS etc.) and low-voltage (circuit breakers, wiring accessories etc.) for data center at a 24% CAGR 2019-23. It now represents 12% of the Electrification segment and ~5-6% of the group. The company offers energy management software for HVAC and energy efficiency as well. As a global leader in Medium Voltage, ABB is also exposed to grid infrastructure investment. ABB targets 5-7% average annual growth for the overall Electrification segment with much higher growth expected from Data Centers.

Schneider (SU – Paris – €207.65)

Based outside Paris, Schneider Electric (SU – FR) is a large French cap global electrical equipment player with a high single digit exposure to Grids and a ~19% exposure (both based on orders) to Data Centers. Schneider sees itself well placed to capture share in the fast growing market for grid products, as it expects 25% of global grid expenditure to target digitization, reflecting customers’ desires for a smarter, reliable and more resilient grid. Schneider’s AVEVA PI system helps grid operators contextualize vast amount of data, supports operations with ADMS and, helps grid operators manage third party assets using DERMS. Schenider’s Data Center portfolio covers the end-to-end design to running of data centers, starting from the creation of a digital model (digital twin) of the data center, to the integration of multiple sources of energy, as well as power distribution, including medium and low-voltage, and power requirements at the rack level. Schneider also supplies asset connectivity for the monitoring layer to ensure seamless operations for the data center. Schneider expects a 10%+ CAGR for the data center market through 2027 and targets 7%-10% organic revenue growth companywide.

Legrand (LR – Paris – €95.54)

Based in Limoges, France, Legrand (LR – FR) is a large French cap global electrical equipment player. It has 15% of group sales coming from data centers, which it aims to expand to 50% over the medium term. Given Legrand’s low voltage focus, 90% of its revenues come from the white room/space of the data center (where IT equipment is placed), and only 10% from the grey room (where back-end infrastructure is placed). For the white space, Legrand’s product offering includes busways, racks, PDUs, containment connectivity and cable management.

ONE CORPORATE CENTER RYE, NY 10580 Gabelli Funds TEL (914) 921-5100