Gabelli Funds hosted its 15th Annual Media & Entertainment Symposium at the Harvard Club in New York City on Thursday, June 8, 2023. The symposium featured discussions with leading companies and organizations across the media ecosystem, with an emphasis on industry dynamics, current trends, and business fundamentals, as well as a Sports Investing Panel. Attendees also had the opportunity to meet with management in a one-on-one setting.

Overview

Broadcasters’ revenue profiles are less dependent on advertising spending and less impacted by the rise of virtual MVPDs than cable networks. The landscape has evolved as scaled players have emerged from consolidation. Broadcasters have been aggressive at driving contractually-recurring retransmission fees, and political advertising dollars are again expected at record levels in the 2024 presidential election cycle. While core advertising is highly volatile during recessionary periods (during the 2008-2009 financial crisis, U.S. advertising saw steep declines of more than 15%), politicians and PACs are generally well-financed. Local TV should be the primary beneficiary of record 2024 presidential election cycle political ad spending, and given low variable costs, political ad dollars generally fall to a pure-play broadcaster’s bottom line. With contractually-guaranteed retransmission revenues and record political advertising spend expected in 2024 broadcasters are better-positioned to withstand a more challenged economic backdrop.

Cord Cutting & Shaving – Pressure Persists: From a peak of over 100 million in 2015, pay TV subs are now under 79 million, and penetration is estimated at ~56% of TV households (down from a peak of 80%). In light of these shifts, the U.S. pay-tv landscape is changing. Virtual MVPDs are becoming increasingly prevalent as younger consumers continue to shave and cut the cord, and these services continue to take share from traditional pay-tv offerings. The growth in virtual MVPD subscribers has helped to offset some of the declines on the traditional MVPD side, although not fully. Retransmission revenues are backed by multi-year contracts, so unless there are a significant number of subscriber cancellations above prior expectations, which remains unlikely at this time, there should be little impact in a more challenged macro environment.

Core Advertising Trends: Broadcasting companies revenue will likely be negatively impacted, at least in the near term, as a result of exposure to advertising. However, the impact is somewhat mitigated by broadcasters’ diversified sources of revenue today, as non-political (‘core’) advertising comprises less than 50% of a pure-play broadcaster’s revenues (as compared to about 90% during the last recessionary period). The economic outlook in the U.S. remains uncertain, and macro dynamics continue to have an impact on corporate advertising and marketing budgets, which are often viewed as discretionary.

2024 Political Advertising Outlook: In contrast to core advertising, U.S. political advertising is again anticipated at record levels during the upcoming 2024 presidential election cycle. Local broadcast stations are uniquely positioned for political advertising given the regional nature of their signals. While digital continues to take share of the total U.S. advertising market, local TV still captures the lion’s share of total political ad spending. Competitive races typically generate the most political advertising revenue, and accordingly, stations reaching markets with those close races should outperform. Strong political this year should help mitigate lingering core advertising demand.

Broadcast Industry Regulations & M&A Activity: On April 20, 2017, the FCC reinstated the Ultra High

Frequency (UHF) discount giving broadcasters with UHF stations the ability to add stations without running afoul of the National Ownership Cap. The current 39% ownership cap is unlikely to change in the near-term. Should the FCC substantially change the ownership cap, we would expect consolidation to accelerate. We would expect both cost reductions and revenue growth, primarily in the form of increased retransmission revenue, to benefit the broadcast stations and networks.

Streaming Wars & Content: The streaming business is in transition. Companies across the industry are dialing back expectations for subscriber growth and the amount that they are willing to spend on content. The major streaming companies spend more than an estimated $120 billion on content in 2022, and we expect to be relatively flat for this year. So far, Netflix is the only streamer that is profitable at scale. The legacy media companies need to figure out an economic model that will lead to profit sooner and offset the declines in their broadcast and cable businesses. Advertising will play a bigger role in the future of streaming, whether that is in Free Ad-Supported TV (FAST) or Advertising-based Video on Demand (AVOD). Recently, Netflix and Disney+ launched AVOD tiers, and AMC Networks will be launching an ad-supported tier of AMC+ later this year.

Theatrical Exhibition: The theatrical exhibition business has been slow to recovery from the COVID-19 pandemic. The domestic box office in 2022 was down 35% versus 2019 at $7.4 billion. Year-to-date, the box office is down 22% compared to 2019. While an improvement, it remains unclear when or if audiences will return at the levels they did prior to the pandemic. The availability of streaming services and alternative sources of entertainment like social media and video games have clearly taken share from movie theaters in recent years.

AMC Networks (AMCX – $11.96 – NASDAQ) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

AMC Networks Inc., an entertainment company, owns and operates a suite of video entertainment products. The company operates in two segments, Domestic Operations, and International and Other. The Domestic Operations segment operates various national programming networks, including the AMC, WE tv, BBC AMERICA, IFC, and SundanceTV; provides subscription streaming services comprising Acorn TV, Shudder, Sundance Now, ALLBLK, and HIDIVE, as well as AMC+ and other streaming initiatives; and engages in film distribution business under the IFC Films name. This segment also produces and licenses original programming for various programming networks, as well as services the national programming networks. The International and Other segment operates a portfolio of channels under the AMCNI name. AMC Networks Inc. was founded in 1980 and is headquartered in New York City.

Reason for Comment

On June 8, 2023, AMC Networks’ CFO, Patrick O’Connell participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· The streaming business is going through a period of rationalization. The industry overspent on programming and marketing. Also, the economic model needs some changes, as fragmentation has increased customer acquisition costs and churn is too high. AMC Networks is reducing the amount they are spending on content and cutting costs to drive towards profitability.

· Bundling is likely the future of streaming. It is unclear who the winners and losers will be in aggregating streaming services, so AMC Networks is open-minded to who they bundle with. However, the technology companies like Amazon are well-positioned to do it.

· The advertising market remains challenging. Advertisers are less willing to spend given the macro uncertainty. However, AMC Networks sees opportunities with the launch of its ad-supported AMC+ tier later this year, as well as the 17 FAST channels the company currently offers.

Summary

AMC Networks management recognizes the need for rationalization in the streaming business. Management is reining in costs and positioning itself for optionality as the economic model evolves. The company continues to have a healthy production and licensing business, like its recent production of the series Silo for Apple TV+.

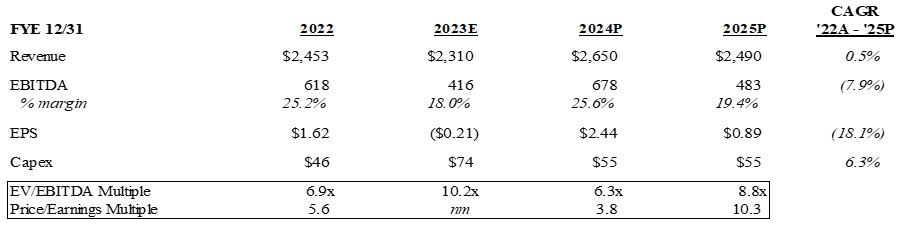

Table 1 AMC Networks Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Beasley Broadcast Group (BBGI – $1.02 – NASDAQ) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Beasley Broadcast Group, a multi-platform media company, owns and operates 61 AM and FM radio stations in 14 large- and mid-size markets across the United States. The company offers local and national advertisers integrated marketing solutions across audio, digital, and event platforms. It also operates Houston Outlaws, an esports team that competes in the Overwatch League, and an esports team that competes in the Rocket League. The company was founded in 1961 and is headquartered in Naples, Florida.

Reason for Comment

On June 8, 2023, Beasley’s Chief Revenue Officer, Tina Murley and Chief Content Officer, Justin Chase presented at our 15th Annual Media & Entertainment Symposium. Highlights from the session are included below:

· Beasley stations reach more than 20 million consumers on a weekly basis. Nearly 41% of Beasley radio properties are located in the nation’s top 50 markets, with the remaining stations primarily in vibrant regional centers. The company has the largest average market share compared to industry peers, according to Nielsen.

· Revenue from company’s foundational business, Audio, continues to increase as a result of Beasley’s unique talent offering community-engaging content. BBGI’s stations are home to a diverse range of formats, featuring top on-air personalities and programming that appeal to a wide range of audiences and demographic groups. In terms of advertising exposure, 74% of the company’s total revenue is local and less than 13% is national.

· Beasley’s Digital division combines the power of local with BMG’s industry-leading digital offerings to deliver results-driven integrated marketing programs for clients. Digital continues to see strong momentum, with revenue growing at 30% CAGR Q1 ’19 – Q1 ’23, and represents almost 20% of total company revenue today.

· Beasley diversified into esports in the fall of 2018 in an effort to create high-quality, cross-platform content for next-gen consumers interested in video games and esports.

Summary

Beasley has positioned itself as the one-stop shop for all local business advertisements. The company’s radio clusters are some of the largest station groups in their respective markets (when ranked by revenue), which helps to enhance each station’s group appeal to the widest range of advertisers and generate operating efficiencies. The digital side of the business continues to see strong growth and accounts for nearly 20% of total company revenue today. Growth in 2024 and beyond will be driven by strategic investment into the expansion and enhancement of digital capabilities.

Table 1 Beasley Broadcast Group Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Comscore, Inc. (SCOR – $0.81 – NASDAQ) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Headquartered in Reston, Virginia, Comscore operates as an information and analytics company that measures audiences, consumer behavior, and advertising across media platforms in the U.S., Europe, Latin America, Canada, and internationally. The company offers a wide range of ratings and planning products and services; custom solutions for planning, optimization, and evaluation of advertising campaigns and brand protection; and provides products that measure movie viewership and box office results. It serves digital publishers, television networks, movie studios, content owners, brand advertisers, agencies, and technology providers.

Reason for Comment

On June 8, 2023, Comscore’s Chief Executive Officer, John Carpenter participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Highlights from the session are included below:

· Media disruption has upended the way marketers and media companies connect with audiences to drive growth. As a pioneering audience measurement company, SCOR was founded with a mission to solve the most complex challenges, and that challenge today is accurately measuring audiences in an increasingly cross-platform world.

· To make decisions with confidence, the world’s leading businesses need an independent partner for understanding consumer behavior across platforms. Comscore’s partners include the largest television networks, digital media properties, brands, agencies, and film studios worldwide.

· SCOR believes it is uniquely positioned to deliver on the opportunity today because of the complete view of audience it has, along with its experience to know what to do with all that data. The company measures more than one trillion events per month across mobile devices, CTV, laptops, mobile apps, and has the ability to measure audiences down to the zip code level, providing targeted audience data with precision.

· Recent business wins include YouTube & NFL Sunday Ticket, Tubi, and Roku with Comscore Campaign Ratings (‘CCR’) as well as Warner Bros Discovery, NBC Universal, and IPG currency expansion.

Summary

Comscore plays an integral role in the media ecosystem today; with transformative data and vast audience insights across digital, linear TV, over-the-top (OTT), and theatrical, the company is a powerful third-party source for reliable measurement of cross-platform audiences.

Table 1 Comscore, Inc. Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Corus Entertainment (CJR.B – C$1.31 – TSX) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Corus Entertainment, located in Toronto, Canada, is a leading media and content company that creates and delivers high-quality brands and content for audiences in Canada and around the world. Founded in 1999 by JR Shaw, the company was built from media assets originally owned by Shaw Communications. Corus’ portfolio of television services includes 33 specialty channels and 15 conventional TV stations, as well as a suite of digital assets. In addition, the company owns 39 radio stations that represent some of the most-listened to stations in Canada. Corus also creates content that is sold in more than 160 countries across the world.

Reason for Comment

On June 8, 2023, Corus’ President & Chief Executive Officer, Doug Murphy presented at our 15th Annual Media & Entertainment Symposium. Highlights from the presentation are included below:

· Corus anticipates Canadian broadcast industry regulatory changes in the near-term. Corus is cautiously optimistic that spending requirements will be reduced (current regulations require broadcasters to spend 30% of prior year’s revenues on Canadian programming). Further, while the CRTC has required broadcasters to make up the COVID period spending shortfalls, this obligation may be reduced or partially relieved as well.

· Management anticipates Corus can deliver modest top line growth in the coming years. Advertising and subscription revenue streams should continue to benefit as Corus takes share and audiences shift, and content licensing revenue is expected to grow at double-digit rates (off a small base). Stack TV, an ad-supported SVOD offering on Amazon, is still targeting one million subscribers, helping to mitigate pressure from cord-cutting.

· Corus continues to invest in technology that advances the company’s strategic priorities. Corus’ superior targeting capabilities allow the company to charge higher CPM rates while providing a more robust offering.

· While Corus continues to drive its various growth initiates, management plans to also remain focused on the company’s cost structure, operating execution, and FCF generation. Even on modest revenue growth, Corus should be able to generate a significant amount of cash and de-lever the balance sheet moving forward.

Summary

Corus remains focused on optimizing its core business and diversifying the company’s revenue base while controlling costs. Corus has strategically prioritized its content business as demand for original programming and spending on high-quality original content continues to increase.

Table 1 Corus Entertainment Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

The E.W. Scripps Company (SSP – $9.15 – NASDAQ) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

The E.W. Scripps Company is a diversified media enterprise and one of the nation’s largest independent owner of television stations in the United States. Scripps’ Local Broadcast Group is comprised of 61 TV stations from coast to coast, including 42 Big Four network affiliates and 10 duopolies. The Scripps Networks reach nearly every American through the national news outlets Court TV and Scripps News as well as popular entertainment brands ION, Bounce, Defy TV, Grit, ION Mystery, and Laff. Scripps is the nation’s largest holder of broadcast spectrum. The company runs an award-winning investigative reporting newsroom in Washington, D.C., and is the longtime steward of the Scripps National Spelling Bee. The company was founded in 1878, and is headquartered in Cincinnati, Ohio.

Reason for Comment

On June 8, 2023, Scripps’ Chief Financial Officer, Jason Combs and Chief Communications & Investor Relations Officer, Carolyn Micheli participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· Scripps has nearly doubled its local television station portfolio in the last several years, and the company’s expanded reach and scale enhances its position ahead of both the critical 2024 midterms and future retransmission negotiations. The company had over 20% and 75% of subscribers reprice in 2022 and 2023, respectively. Management believes there is still ample room for growth on rate moving forward.

· Scripps also made the large acquisition of Ion Media in early 2021, combining it with Scripp’s eight legacy national networks. The company does not currently expect them to be up in light of the larger advertising recession.

· Political advertising is expected to be robust again industry-wide in 2024, and Scripps has an exceptionally strong footprint. Accordingly, the company is uniquely positioned to capture these high-margin dollars. Management anticipates 2024 political will at least meet, and may even exceed prior presidential cycle records.

· In terms of over-the-air (‘OTA’), roughly a third of all U.S. households today use digital antenna, and viewers get about two- to three-dozen free channels (including all eight Scripps networks). So the more people seeking free TV, the more people that will find Scripps’ offerings.

Summary

While the current softness in advertising spend creates certain challenges, Scripps is better-positioned to weather an advertising recession today than the company was in prior periods. The company has solid visibility into its contractually-backed retransmission revenues for the next several years, and the industry continues to expect record political spending during the 2024 presidential election cycle.

Table 1 The E.W. Scripps Company Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Gray Television (GTN/’A – $7.88 – NYSE) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Gray Television, headquartered in Atlanta, GA, is television broadcast company and the largest owner of top-rated local TV stations and digital assets in the United States. In January 2019, Gray nearly doubled its size through the acquisition of Raycom and, in 2021, expanded further with the acquisitions of both Quincy Media and Meredith’s local TV station portfolio. The company’s stations serve 113 television markets that collectively reach approximately 36% of U.S. television households. Gray also owns video program companies Raycom Sports, Tupelo Media Group, PowerNation Studios, as well as the studio production facilities Assembly Atlanta and Third Rail Studios. The company primarily generates revenue from broadcast and internet advertising and retransmission consent fees and also owns video program production, marketing, and digital businesses.

Reason for Comment

On June 8, 2023, Gray Television’s Chief Financial Officer, Jim Ryan participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· Gray’s stations are typically the #1 or #2 in the markets where it operates, and the company’s strong rankings position it favorably both with advertisers as well as distributors and networks.

· As retransmission, political, and digital sources of revenue continue to grow and take share of the company’s overall revenue mix, Gray has become less-reliant on core advertising, which tends to be volatile.

· The intensely polarized political landscape and number of competitive races continues to drive high-margin political advertising spend industry-wide, and management is optimistic that 2024 political could approach record 2020 levels. Gray has a strong footprint for the 2024 presidential cycle and, with significant exposure to many of the most competitive races, is well-positioned to benefit.

· Larger-scale broadcast M&A and regulatory changes are unlikely in the current environment.

Summary

Gray’s outlook for political advertising and retransmission revenues remain solid despite a more challenging core advertising market, especially on the national side. Furthermore, Gray’s more recent acquisitions improve its position ahead of the critical 2024 political cycle, and the company should be able to capture additional political and retrans dollars with its increased scale.

Table 1 Gray Television Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Grupo Televisa (TV – $5.13 – NYSE) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Grupo Televisa, S.A.B. operates through three segments: Cable, Sky, and Other Businesses. The Cable segment provides video, broadband, and mobile connectivity to nearly 16 million revenue-generating units (RGUs) throughout Mexico. Sky (owned 59% / 41% by Televisa / AT&T) provides satellite pay television, fixed, and mobile broadband to over six million customers in Mexico, Central America, and the Dominican Republic. Other Businesses include the Club America soccer team and Azteca stadium, magazine publishing and distribution, and gaming. Televisa intends to spin-off most of the assets in this segment. In addition, Televisa holds a 44% stake in TelevisaUnivision (TU) resulting from the January 2022 combination of its Mexican content production and distribution businesses with Univision’s US broadcasting operations. TU has launched Vix, the largest dedicated Spanish-language direct-to-consumer service, globally.

Reason for Comment

On June 8, 2023, Grupo Televisa’s co-CEO, Alfonso De Angoitia, and VP of Finance Carlos Margain participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· The deal to combine TV’s media assets with Univision to form TelevisaUnivision is transformational, creating the leading media company for the Spanish language market. There are 600 million Spanish speakers in the world, representing $8 trillion of GDP.

· The Vix streaming service has grown to over 30 million monthly active users in less than a year. It offers a single platform for the premium SVOD service and free ad-supported service.

· The cable business is the largest in Mexico and generates more than $1 billion in EBITDA. Broadband penetration in Mexico is still low at around 70% vs 95% for the US and 85% for the rest of Latin America.

· The ad market in the US is softer than in Mexico. The upfront cycle occurs later in the year than in the US, so there is still time to work through this downturn before the next cycle begins. TelevisaUnivision has also outperformed the general market by 800 basis points.

Summary

We believe that Grupo Televisa’s stake in TelevisaUnivision is a unique asset in the streaming industry, with its focus on the Spanish-speaking market globally. An IPO of that business could be a catalyst for the company in the next 12-18 months. In addition, another attempt at a transaction with Megacable could create value for shareholders.

Table 1 Grupo Televisa Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

IMAX Corporation (IMAX – $61.99 – NYSE) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

IMAX Corporation is a global entertainment technology company. It offers cinematic solutions through proprietary software, theater architecture, intellectual property, and specialized equipment. The company offers IMAX Digital Re-Mastering (DMR), a proprietary technology that digitally enhances the image resolution, visual clarity, and sound quality of motion picture films for projection on IMAX screens; IMAX theater systems to exhibitor customers through sales, leases, and joint revenue sharing arrangements; and digital projection systems. The company’s technology comes together to deliver “The IMAX Experience,” a premium theatrical experience for theatergoers. As of December 31, 2022, the company had a network of 1,716 IMAX theater systems comprising 1,633 commercial multiplexes, 12 commercial destinations, and 71 institutional facilities operating in 87 countries and territories. IMAX Corporation was founded in 1967 and is headquartered in Mississauga, Canada.

Reason for Comment

On June 8, 2023, IMAX’s CFO Natasha Fernandes participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· IMAX is pleased with their box office year to date, and management is guiding to about $1.1 billion for the full year. This gets the company back around 2019 levels, while the rest of the industry is forecast to be 20-30% below 2019. The company has benefitted from increasing premiumization that moviegoers demand to draw them back inside theaters.

· International markets remain a focus for growth. The company has recently signed deals for new screens in markets like India and Indonesia. Local languages films have helped IMAX round out their slate in markets like China and India.

· The company has a handful of initiatives outside of its core business including SSIMWAVE, IMAX Live and IMAX Enhanced, that offer potential upside optionality. SSIMWAVE, a streaming technology company that IMAX acquired in 2022, is particularly interesting and an area of focus for management.

Summary

IMAX currently trades at 8.1x 2024P EBITDA. We view it as a good house in a bad neighborhood, with the company’s box office expected to approach 2019 levels this year versus the larger industry down ~20%.

Table 1 IMAX Corporation Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

The Marcus Corporation (MCS – $14.83 – NYSE) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

The Marcus Corporation, founded in 1935 and headquartered in Milwaukee, Wisconsin, is a Midwestern theater, hotel and resort operator with locations primarily in Midwestern states. Marcus Theaters owns and operates 1,064 screens at 85 locations in 17 states and is the fourth-largest theater circuit in the US. The company offers an array of premium experiences including DreamLounger recliner auditoriums and premium large format (PLF) screens, both of which are offered in 78% of their theaters. The company also offers a customer loyalty program called Magical Movie Rewards with over 5 million members that drive 45% of all box office transactions. The Hotels & Resorts segment consists of seven wholly-owned and operated properties and nine managed properties, for a total of 4,900 rooms.

Reason for Comment

On June 8, 2023, Marcus’ CEO Greg Marcus and CFO Chad Paris participated in a fireside chat at the 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· While the box office is still down this year versus 2019, management remains pleased with the trends in the release schedule and the box office that is being generated. Marcus is increasing the number of premium large format screens in their theaters, in response to demand for experiences that cannot be matched at home. The company is focused on their own proprietary format as it allows for more flexibility and multiple screens per location.

· As the labor market has eased, the company is able to better staff theaters and hotels. This is positive for the business longer term but has increased costs versus the prior year.

· Management believes that the market underappreciates the value of the company’s real estate portfolio, and will look for ways to surface that value.

Summary

Marcus currently trades at roughly 5.6x 2024P EBITDA. We believe that the ongoing recovery in the theatrical box office will help grow revenue and EBITDA. Also, surfacing value in the real estate portfolio should benefit the stock.

Table 1 The Marcus Corporation Earnings Model 2022A – 2025P

Source: Company data and ThomsonOne consensus estimates.

Paramount Global (PARAA – $18.56 – NASDAQ) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Paramount Global, headquartered in New York City, operates as a media and entertainment company worldwide. The company distributes a schedule of news and public affairs broadcasts, and sports and entertainment programming; acquires or develops, and schedules programming on the CBS Television Network that includes primetime comedies and dramas, reality, specials, kids’ programs, daytime dramas, game shows, and late night programs; produces or distributes talk shows, court shows, game shows, and newsmagazines; owns and operates 29 broadcast television stations; and operates CBS Sports Network, a 24-hour cable channel that provides sports and related content, as well as streaming and cable subscription services. It also operates Paramount+, a digital subscription video on-demand and live streaming services; and creates and acquires programming for distribution and viewing on various media platforms, including subscription cable networks, subscription streaming, and premium and basic cable networks. In addition, the company develops, produces, finances, acquires, and distributes films.

Reason for Comment

On June 8, 2023, Paramount Global’s CFO Naveen Chopra participated in a fireside chat at the 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· Paramount is optimistic in the recovery in the advertising market, as soon as the back half of this year.

· The company has been ahead of the industry on bundling its streaming service with other products, like Walmart+ and Delta. We expect bundling to expand within the streaming industry as companies look for ways to lower customer acquisition costs and reduce churn. Paramount recently merged Paramount+ with Showtime to build further scale for Paramount+, and drive efficiencies through lower content spending and other costs. The company also used this combination as an opportunity to increase the price for the premium ad-free tier from $9.99 to $11.99 a month.

Summary

Paramount currently trades at 8.3x 2024P EBITDA, at the lower end of public comps like NFLX and DIS, but at a premium to WBD. The company expects peak DTC losses to occur this year with EBITDA and cash flow improving starting in 2023. The company is open to potential transactions involving its assets, including the announced process for Simon & Schuster.

Table 1 Paramount Global Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Reading International (RDI – $2.65 – NASDAQ) Symposium Highlights

COMPANY OVERVIEW

Reading International, Inc. located in Los Angeles, CA, is a real estate and theatrical exhibition company with operations in the U.S., Australia, and New Zealand. The Cotter Trust owns 69% of the outstanding Class B Stock and, as a result, controls ~69% of the voting power of the company. The company leverages its theater cash flow into developing the underlying owned real estate. The Cinema Exhibition segment owns or manages 62 locations (fee interest in 12) with 405 screens in between: U.S. – 23 theaters (tenth-largest chain), Australia – 27 theaters (fourth-largest chain), and New Zealand – 12 theaters (third-largest chain). The company operates modern stadium seating multiplexes, specialty art house theaters (Angelika), and conventional sloped floor theaters. Reading International is upgrading its theatres to offer recliner seating and a full range of food and beverages. The Real Estate segment includes ownership or long-term leaseholds of properties used in the Cinema Exhibition activities, acquisition of land for general development, and redevelopment of properties such as 44 Union Square in New York City.

Reason for Comment

On June 8, 2023, Reading International’s Executive Vice President of Global Operations Andrzej Matyczynski presented at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· Management highlighted their dual business strategy of operating movie theaters and real estate development across the US, Australia and New Zealand.

· Reading has been renovating and upgrading theaters across its circuit, and enhancing its food & beverage offering. As a result, patron per capita spending has grown. For example, in the US it has grown from $5.52 in 2019 to $7.60 in 2022.

· The property at 44 Union Square is now 42% occupied by Petco, and the company is looking to lease out the remaining space in the building. Also, Reading recently announced that it would be pursuing a sale lease-back of its headquarters in Culver City, California to help shore up its balance sheet.

Summary

Reading is currently free cash flow negative while its theaters are still recovering. As a result, the company will be selling its headquarters to raise cash. Reading sits on a portfolio of under monetized real estate assets could be sold and unlock value if management chose to do so.

Table 1 Reading International Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Sports Investing Panel Symposium Highlights

We hosted Sal Galatioto, president of Galatioto Sports Partners, Michael Ozanian, Assistant Managing Editor of Forbes Media, and Michael Levine, Co-Head of CAA Sports for an engaging discussion on current trends in the sports business landscape.

Key Takeaways

· Rights to live sports will continue to grow in value as sports remains one of the last types of content that is primarily viewed live. Rights owners will be indifferent to the channels of distribution as long as prices are going up. The national and global sports media landscape is healthy despite what may look like a bubble.

· The RSN model is in transition, and the leagues will take advantage of the opportunity to shift the business model.

· The NHL landscape is expected to shift, with teams relocating and expanding. There was hope that a team would come to Salt Lake City, as well as other cities in Canada.

· Private equity ownership of franchises has expanded the opportunity for investors to access the asset class. The panelists expect the NFL to open up to private equity ownership once a deal is done for the Washington Commanders. This will be a tailwind for the industry as there will be more demand for teams, and there will be more ownership groups that own more than one team. These buyers view teams as intellectual property and will be valued on revenue multiples like successful technology companies.

· There are risks to the legalization of sports gambling, but so far it is working. If fans have money on the game, they will be more engaged. The gambling apps are very compelling and dynamic, and allow people to wager on events and moments within games.

· The decision by Major League Baseball to add the pitch clock is one of the smartest things that they ever did. It makes the games faster, more exciting, and more engaging for fans.

· Formula One is a global juggernaut, driven in part by the Netflix series Drive to Survive. It will be rare to see F1 teams sold entirely, but you will see more minority owners coming into the sport.

· It was not a surprise to see the PGA and LIV merge. It is a big moment for the sport, but they mishandled the communication with the players. However, as more money pours in from the PIF, the unrest from players will die down. In general, more money from Saudi Arabia will come into sports going forward.

· The NIL landscape is very broken, and it will take an act of Congress to fix it.

Summary

We continue to see attractive opportunities in owning sports teams and leagues going forward. The leagues are open to a wider range of buyers than in the past, expanding the pool of capital available to buy teams. This should be a tailwind to valuations. Sports broadcast and streaming rights also remain an important asset as sports programming is one of the last types of programming that viewers are tuning in to live. This drives strong engagement by viewers and an opportunity for advertisers to reach their customers. However, the RSN model is in flux as more subscribers cut the cord and fewer people pay for their local RSN.

TEGNA Inc. (TGNA – $16.24 – NYSE) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

TEGNA Inc., headquartered in Tysons, VA, owns and operates 64 television stations and two radio stations in 51 U.S. markets. The company is the largest owner of Big Four network affiliates in the top 25 markets, reaching ~39% of all television households nationwide. TEGNA also owns leading multicast networks True Crime Network, Twist, and Quest. TEGNA offers innovative solutions to help businesses reach consumers across television, digital, and over-the-top (OTT) platforms, including Premion, the company’s OTT advertising service.

Reason for Comment

On June 8, 2023, TEGNA’s President & CEO, Dave Lougee and CFO, Victoria Harker participated in a fireside chat at our 15th Annual Media & Entertainment Symposium. Discussion highlights are included below:

· TEGNA recently concluded a year-long plus merger process with Standard General, which was ultimately terminated. The company has an industry-leading balance sheet, with net leverage under 3x, and expects to remain comfortably within the 2x’s range, even after returning significant capital to shareholders this year.

· Following the deal termination, TEGNA announced a $300 million ASR (expected completion: end of Q3 ‘23), and the company has also opted to take its $136 million breakup fee from Standard General in the form of shares. TEGNA’s board has also approved a 20% increase in its quarterly dividend, to 11.375 cents vs. prior 9.5 cents.

· The industry is anticipating another record political cycle in 2024, and TGNA has a solid footprint. Additionally, the Super Bowl will return to CBS in 2024, and the Olympics will air on TEGNA-operated channels.

· On the network affiliate side, the company will be negotiating deals for 60% of its subscriber base up for renewal at year-end. Management expects network compensation (payments back to the networks) will decline moving forward, reflecting the recent shifts to less-exclusive content. Accordingly, net retrans margins are expected to improve moving forward from there.

· TEGNA remains open to future M&A opportunities and expressed interest in participating in further industry consolidation on both the buy- and sell-side moving forward.

Summary

TEGNA has solid visibility into the company’s contractually-backed retransmission revenues through 2025, and the industry continues to expect record political advertising for the 2024 presidential election cycle. The company has an industry-leading balance sheet, and expects to remain comfortably within the 2x’s leverage range, even after returning significant capital to shareholders this year. In our view, TEGNA is the last public consolidation target remaining in broadcast, and we anticipate the company will continue to participate in M&A in the future.

Table 1 TEGNA Inc. Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.

Townsquare Media (TSQ – $11.91 – NYSE) Symposium Highlights

Source: Company data and ThomsonOne consensus estimates.

COMPANY OVERVIEW

Townsquare is a community-focused digital media, digital marketing, and radio company focused outside the Top 50 markets in the U.S. The company’s assets include Townsquare Interactive, a digital marketing services subscription business providing websites, search engine optimization, social platforms, and online reputation management for nearly 30,500 small businesses; Townsquare IGNITE, a proprietary digital programmatic advertising technology with an in-house demand and data management platform; and Townsquare Media, a portfolio of 357 local terrestrial radio stations in 74 U.S. cities with corresponding local news and entertainment websites and apps.

Reason for Comment

On June 8, 2023, Townsquare’s Chief Executive Officer, Bill Wilson and Chief Financial Officer, Stuart Rosenstein presented at our 15th Annual Media & Entertainment Symposium. Session highlights are included below:

· Townsquare Media’s strong and fast-growing digital businesses with profitable revenue streams are supported by the mature, ‘cash cow’ local radio broadcast business with very strong cash flow characteristics.

· TSQ recently re-segmented the business (beginning with FYE 2021 reporting) to better align with how management views the company and its strategy today. This provides relevant data to allow a sum-of-the-parts valuation for the company’s high growth and subscription-based digital businesses.

· The company’s presence and disciplined focus outside the Top 50 U.S. markets is a competitive advantage, given the greater need for local content in markets outside the largest cities and a much weaker digital competitive landscape. Townsquare generally operates in healthy, stable markets with lower economic volatility and stabilizing institutions such as universities, military installations, and state capitals.

· The digital audience to TSQ’s owned & operated properties is ~6.8x the size of its terrestrial radio audience today, and ~20% of total net revenue is monthly, recurring subscription digital marketing revenue. By 2024, the company expects to generate a minimum of $275 million of digital revenue, at least +9% CAGR from 2022.

Summary

Townsquare Media has successfully transformed into a digital-first local media company, with 50%+ of all profit and revenue generated from recurring, subscription digital marketing solutions and digital advertising, which are greatly differentiated vs. local digital agencies or other competitors. The company has invested in leading technology and infrastructure to serve a broad base of local businesses and engage its loyal audiences and communities.

Table 1 Townsquare Media Earnings Model 2022 – 2025P

Source: Company data and ThomsonOne consensus estimates.